The One Money Habit That Separates Couples Who Build Wealth

There is a pattern that shows up consistently in personal finance research, and it has almost nothing to do with income. The couples who end up in the strongest financial position are not necessarily the highest earners. They are the ones who have a shared direction. A common understanding of what their money is for, where it is going, and what they are building together.

That sounds obvious. In practice, very few couples actually have it.

Most share a home, a mortgage, and daily expenses. But the financial strategy behind all of that, the savings rate, the pension choices, the ISA usage, the spending patterns, tends to be handled separately, quietly, and without much conversation. Not because anyone is hiding anything. Because money conversations feel heavy, and there is always something more pressing to deal with.

The cost of that gap is not dramatic. It is slow. It shows up over years in unused tax allowances, misaligned pensions, and savings sitting in the wrong places.

What most people do wrong

The default for most couples is a rough split of responsibilities. One person handles the mortgage and bills. The other manages groceries and daily spending. Both assume the other is doing something sensible with whatever is left over. Nobody checks. Nobody asks.

Research from Legal and General found that nearly half of UK adults consider money too personal to discuss, even with a partner. One in ten people in relationships admitted to not being fully honest about their finances. Eight percent did not know what their partner earned.

The result is two people running a shared household on separate financial assumptions. Sometimes those assumptions line up. Often they do not. And the longer the gap goes unexamined, the more it compounds.

The issue is not trust. It is structure. Without a shared view of the numbers, it is very difficult to make good decisions about pensions, tax, savings, or investing as a household rather than as two individuals.

What is actually happening

A couple in the UK has access to a combined ISA allowance of £40,000 per year. If only one partner is using theirs, the household is leaving up to £20,000 of tax-free investment space on the table every year. Over a decade, the compounding cost of that unused allowance is significant. We explain how the ISA wrapper works in a separate article.

Pensions are another area where household-level thinking changes the picture. If one partner is contributing above the employer match into a global equity fund and the other is on the default minimum going into a cautious lifestyle fund, the long-term difference in outcomes can be tens of thousands of pounds. It is not enough for one partner to have a good pension strategy. Both need to be in a reasonable position, because retirement is usually a shared event. Our article on why most pensions are in the wrong fund covers how to check.

Tax planning works the same way. If one partner earns below the personal allowance, they can transfer £1,257 of it to the other via the marriage allowance, saving £252 per year. Over two million eligible couples in the UK do not claim it. If one partner earns near £100,000, pension contributions via salary sacrifice can protect the personal allowance and save thousands. These are decisions that only make sense when you look at both incomes together.

None of this is complicated in isolation. The difficulty is that it requires both people to sit down, look at the same numbers, and talk about them.

What we found

We try to sit down together every four or five months and go through everything properly. Not a quick glance at the bank balance. A proper look at what we have earned, what we have spent, where savings are sitting, what our pensions are doing, and whether the budget allocation still makes sense.

It is always a struggle to find the time. There is always something else that feels more urgent. But the clarity that comes from doing it is worth more than the hour it takes. Every time we have had that conversation, something has come out of it that would not have surfaced otherwise. An account paying the wrong interest rate. A pension contribution that needed adjusting. A spending category that had drifted higher than either of us realised.

The single most useful thing that changed was agreeing on a direction. Not a detailed budget that tracks every pound, but a shared understanding of what we are trying to do. How much we want to save each month. What the money is for. When we expect to need it. Having that shared context means daily decisions do not need to be negotiated. The direction handles it.

The couples who build wealth consistently tend to share three things: a view of their combined net worth, an agreed savings rate, and a plan for their pensions and ISAs that accounts for both incomes. It does not need to be perfect. It needs to exist.

What to do

Step 1. Set a date to sit down together with every financial account visible. Current accounts, savings, ISAs, pensions, credit cards, loans. Both of you. The goal is not judgment. It is a snapshot of where things stand right now.

Step 2. Check both pensions. Log in, find the fund name, check the five-year performance. If either is in a default fund returning less than 5% over that period, it is worth investigating a switch. Our article on checking your pension fund explains how.

Step 3. Check whether you are eligible for the marriage allowance. If one partner earns below £12,570 and the other is a basic rate taxpayer, this is £252 per year and you can backdate it four years. It takes ten minutes to apply online.

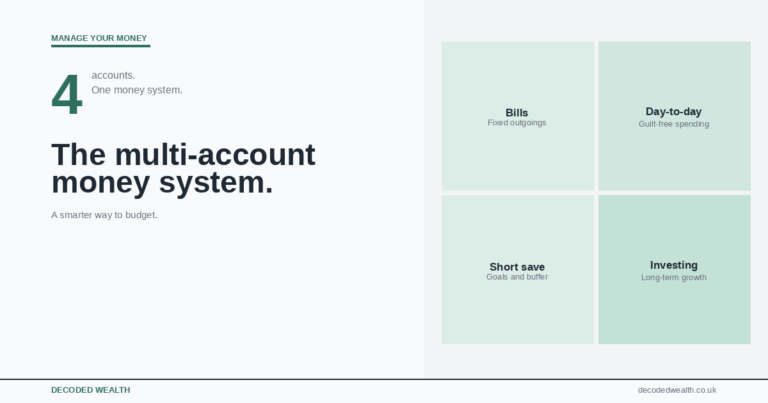

Step 4. Agree on a savings rate and a system. The specific number matters less than the fact that you have agreed on it together. If you need a starting framework, our multi-account system separates money into bills, daily spending, short-term saving, and investing so both partners know where things are without tracking every transaction.

Step 5. Put a recurring reminder in the calendar, every four or five months, to do this again. It does not need to be long. An hour with a laptop, two cups of tea, and an honest look at the numbers. That rhythm is worth more than any single financial decision.

Income gets all the attention. Alignment is the thing that actually determines whether a household builds wealth or just earns it and watches it spread thin. It is not about budgeting harder. It is about both people looking at the same map.

Capital at risk. Investments can go down as well as up. This article is for informational purposes only and does not constitute financial advice. Decoded Wealth is not regulated by the FCA. Always do your own research before making financial decisions. This article may contain affiliate links. If you use them, we may earn a small commission at no extra cost to you.