Why You Still Feel Broke on a Good Salary in the UK (The Hidden Reason You’re Not Building Wealth)

Let us say something that does not get said enough: a 100,000 pound household income in the UK in 2025 is not what it used to be.

Ten years ago that felt like serious money. And it is still a good income, we are not pretending otherwise. But after income tax, National Insurance, student loan repayments, a mortgage that has gone up with interest rates, childcare that costs more than most people’s rent, and an inflation run that made everything from food to energy to insurance more expensive, the take-home reality of a six-figure household is much tighter than the headline number suggests.

So if you are earning decent money and still wondering where it all goes, the problem is almost certainly not that you are bad with money. It is that the cost of a normal life has gone up significantly, and a pattern called lifestyle inflation has quietly eaten the rest.

We have felt this ourselves. And working through it changed how we think about money more than almost anything else.

What lifestyle looks like in real life

Lifestyle inflation is simple. This is the trap most people are in, and it is not always obvious when it is happening.

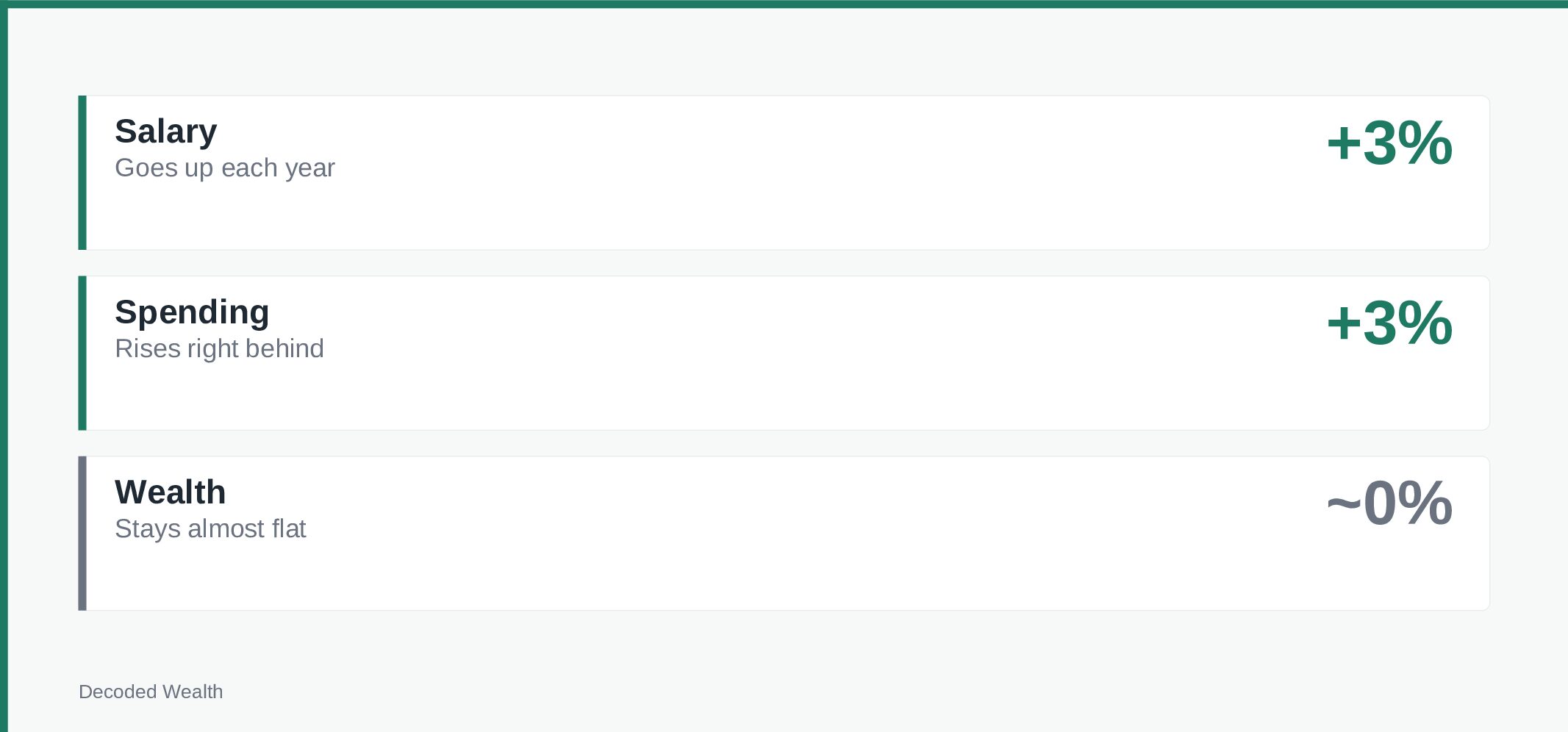

Every time your income goes up, your spending goes up to match it. You get a 3 percent pay rise and within a few months the extra money has been absorbed. A slightly nicer holiday. Eating out a bit more. Upgrading the car when the lease ended rather than keeping the old one. A subscription here, a membership there.

Nothing looks excessive. But together, it leaves very little room for anything else. This is exactly why having a simple system for structuring your money makes such a difference.

That is what lifestyle inflation looks like in practice.

None of these individual decisions are stupid. The problem is the pattern. If every single increase in income immediately becomes an increase in spending, your financial position does not actually improve. You earn more, you live better in the short term, and you have almost nothing more to show for it in terms of savings, investments, or actual wealth.

This is the trap most people are in, and it cuts across income levels. It is not just high earners. It is anyone whose spending automatically scales with their income rather than staying relatively flat while the gap between income and spending gets wider and put to work.

The UK version of this is particularly brutal right now

The last few years have made lifestyle inflation worse because the baseline cost of living went up sharply for everyone. Energy, food, mortgages, insurance. You were not upgrading your lifestyle, you were just paying more for the same things. That is a different problem.

But layered on top of that, many people did also upgrade their lifestyle as incomes rose, because that is what feels natural. You earn more, you should be able to enjoy more. And you should. The question is whether the upgrade is proportionate or whether it has swallowed everything.

A household earning 80,000 pounds gross in the UK takes home roughly 55,000 to 58,000 pounds after tax and National Insurance, less if there are student loan repayments. That is around 4,600 to 4,800 pounds a month. Subtract a London or South East mortgage, two lots of childcare, two cars, utilities, food, insurance, and the usual subscriptions and you are looking at discretionary income that might surprise you with how little it is.

That is not comfortable. That is tight. And the answer is not to feel guilty about your income. It is to be deliberate about what happens to what is left.

The mantra we actually live by

Live below your means. We know, it sounds obvious. It sounds like something your grandparents would say. But there is a version of it that is not about deprivation and is not about refusing to enjoy your life.

It is simply this: do not automatically upgrade your lifestyle every time your income goes up.

When you get a bonus, do not spend it. Or spend part of it and invest the rest. When you get a pay rise, keep your monthly spending roughly where it is and redirect the increase. When a fixed cost like a loan finishes, do not replace it with a new one. Let the cash flow improve and put the difference somewhere useful.

You are not giving anything up. You are just not taking on new spending before you have taken care of your financial future. The lifestyle upgrades can come later, from the returns on your investments, from genuine wealth rather than from this month’s salary.

This one habit, keeping lifestyle costs relatively flat as income grows, is the single biggest differentiator between people who build wealth over time and people who earn well and have nothing to show for it at 50.

Short-term satisfaction vs long-term wealth

We are all wired for the short term. The new car feels good now. The holiday is happening in three weeks. The restaurant booking is tonight. The return on an investment made this month will not be visible for years.

This is not a character flaw. It is human. But wealth is built in the gap between what you could spend and what you choose to spend, and that gap only exists if you protect it deliberately.

A practical way to think about it: before any significant discretionary spending, ask yourself whether you have already taken care of your pension contribution, your ISA contribution, and your savings target for the month. If yes, spend the rest without guilt. If not, the spending comes at the expense of your future self.

That is not restriction. That is priority. Pay your future self first, then enjoy what is left.

The specific things worth checking

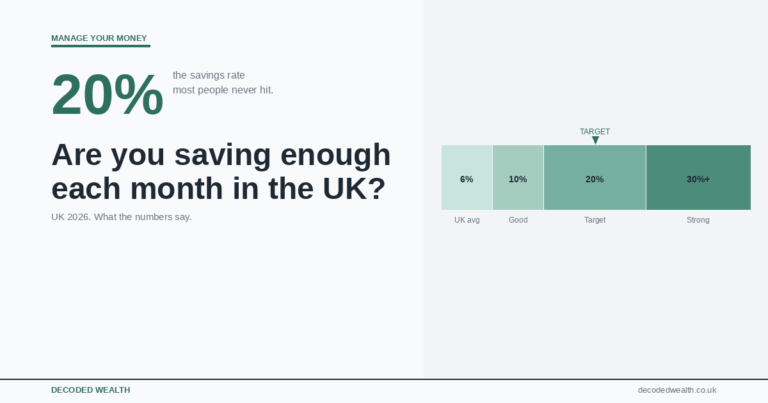

Your actual savings rate: Take everything you save or invest in a month, including pension contributions, and divide it by your take-home pay. If you earn well and the number is under 15 percent, something is absorbing money that should be going elsewhere. The target most financial planners use is 20 percent or more.

Your fixed costs: List every committed monthly outgoing. Mortgage, subscriptions, car payments, insurance, memberships. Add them up. Most people are surprised by the total. Some of these are worth every pound. Others are habits from an earlier income level that stuck around when spending went up.

What happened to your last pay rise or bonus: Be honest. Did it change your financial position materially, meaning more invested, more saved, debt reduced? Or did it get absorbed into spending within a few months? The answer tells you a lot.

Your pension contribution: If you are a higher rate taxpayer, pension contributions are one of the most tax-efficient things you can do. Every pound you put in costs you 60 pence in real terms after 40 percent tax relief. If you are not contributing as much as you comfortably can, you are leaving a significant benefit on the table.

You do not need to earn more. You need to keep more of what you already earn.

That is the shift. Not a bigger salary, not a side hustle, not a windfall. Just a deliberate decision not to let every income increase disappear into spending before it has a chance to become something more useful.

We are not saying never spend. We are saying spend intentionally, after you have taken care of what matters. The things that make life good do not require spending everything you earn. And the things that create genuine financial freedom require spending less than you earn, consistently, over time.

If you want to understand where to put what you save, our seven-step wealth-building order is a good place to start. And if you want to understand how to start investing what you are keeping, our investing guide is the next step.

Capital at risk. Investments can go down as well as up. This article is for informational purposes only and does not constitute financial advice. Decoded Wealth is not regulated by the FCA. Always do your own research before making financial decisions. This article may contain affiliate links. If you use them, we may earn a small commission at no extra cost to you.