Investing in the UK: Is Now Still the Right Time?

We remember the evening we actually started. Not the evening we talked about starting, or the evening we read another article about starting, or the evening we compared platforms for the third time without opening any of them. The evening we sat at the kitchen table, opened a laptop, and created an account.

It took about twenty minutes. It felt like it had taken three years.

Because that is roughly how long we had spent thinking about it before we did anything. We were several years into our careers by the time we made our first investment. And we had a growing, uncomfortable feeling that it was already too late to start investing at all, that everyone around us had started years earlier and we had missed the window.

We had not missed it. But it took a long time, and some painful months of watching our money go down, before we understood that.

What most people do wrong

The biggest mistake is not picking the wrong fund or the wrong platform. It is never starting at all.

The second biggest mistake is starting the wrong way because you think investing means picking stocks.

We made both, in sequence.

For months we researched. We compared platforms. We read about index funds, individual shares, dividend stocks, growth stocks, and things we barely understood. We told ourselves we were being careful. In reality we were being afraid. The volume of information made it easy to convince ourselves we were not ready yet, that we needed to understand one more thing before we could begin.

When we finally did open an account, we did what felt like real investing. We picked individual stocks. Companies we had read about, names we recognised, things that sounded like good ideas at the time. We put small amounts into four or five of them and checked the app constantly.

Within a few months, we were down. Not by a catastrophic amount, but enough to make us question everything. One stock dropped 18%. Another drifted sideways doing nothing. The portfolio as a whole was negative, and we had no framework for understanding whether that was normal or whether we had made a serious error.

That experience is what stops most people. Not the loss itself. The feeling of having tried, having got it wrong, and not knowing what to do next. The instinct at that point is to close the app, leave the money where it is, and go back to thinking about it rather than doing anything about it.

We nearly did exactly that.

What is actually happening

The maths of starting late is not as punishing as most people assume. It is not free either. But the gap between starting now and not starting at all is vastly larger than the gap between starting now and having started five years ago.

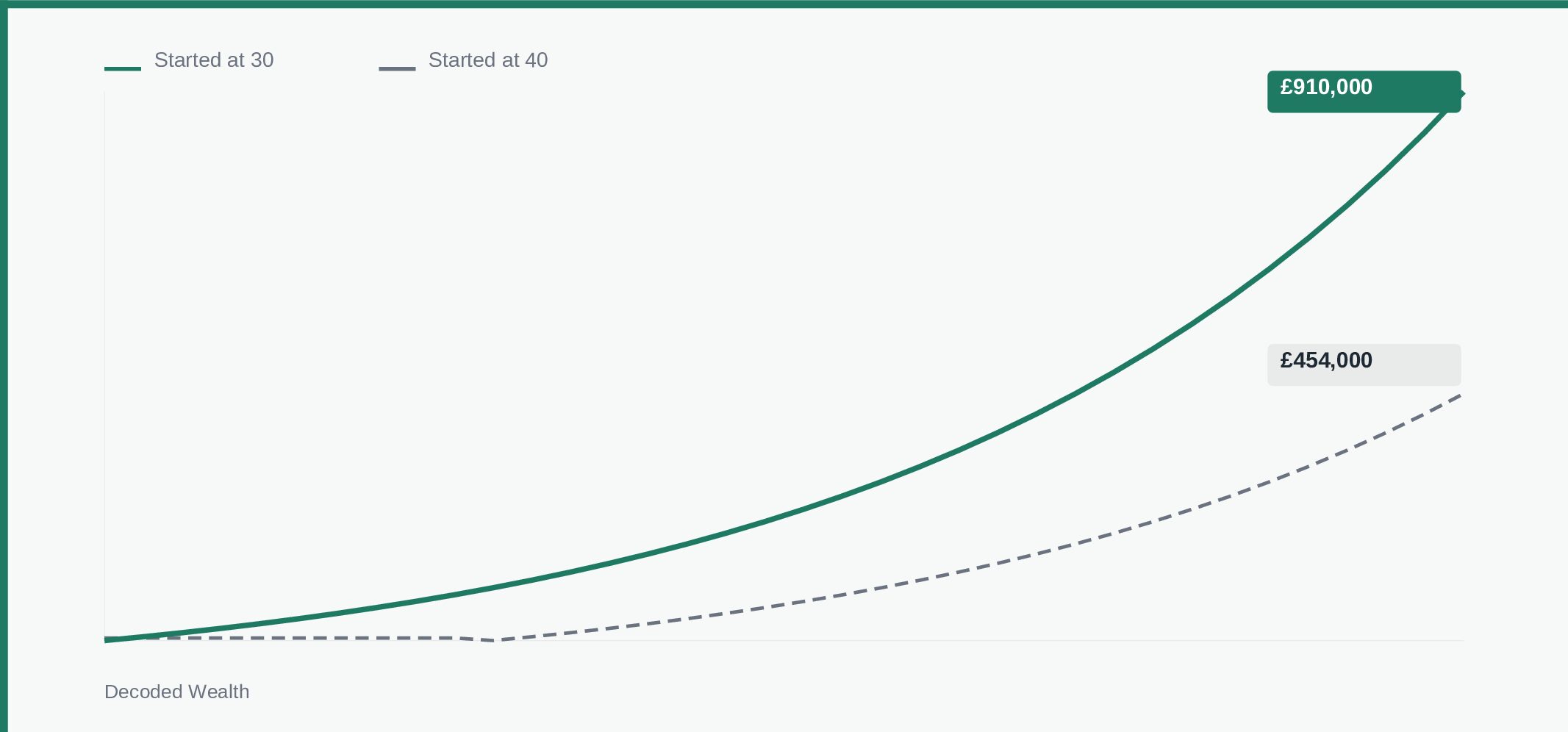

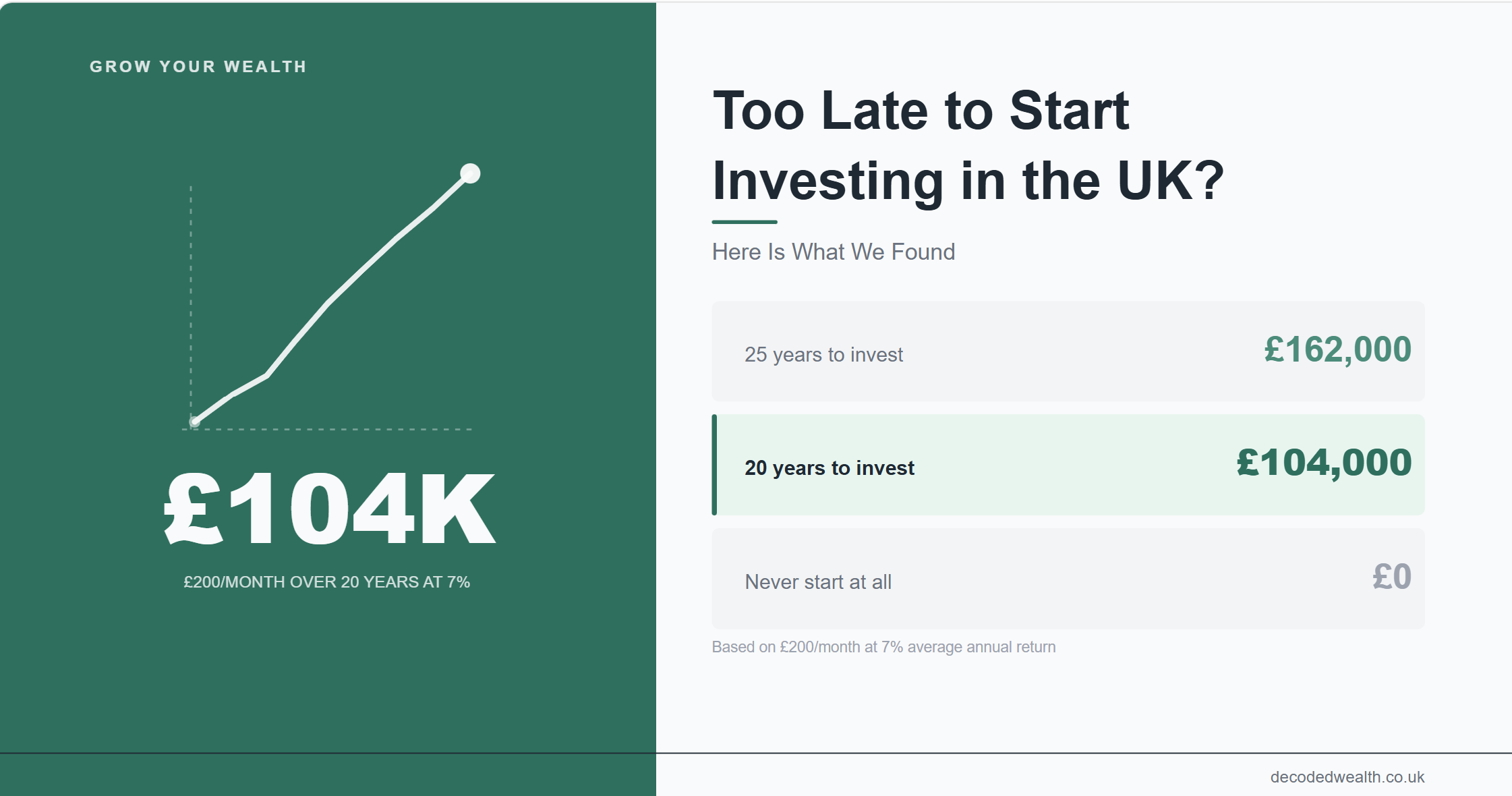

Here is what £200 per month looks like invested at an assumed average annual return of 7%, which is broadly consistent with long-term global index fund performance based on historical data from providers including Vanguard.

Starting with 25 years of investing ahead, the pot grows to approximately £162,000. Starting with 20 years, roughly £104,000. Starting with 15 years, around £63,000. Starting with 10 years, approximately £35,000.

The difference between 25 years and 20 years is about £58,000. That is real money. But the difference between 20 years and never starting is £104,000. The person who starts five years later than they wanted to is not in a disastrous position. The person who never starts is.

There is another number that matters. A single lump sum of £5,000 invested at the same 7% average return grows to roughly £19,300 over 20 years without adding another penny. That is the compounding effect working on one deposit. Every year you leave money uninvested in a current account, you are not just missing out on one year of returns. You are missing out on every year of compounding that would have followed.

The other thing the maths reveals is that what you invest in matters more over time than when you started. A person who begins five years late but invests in a diversified global index fund with low ongoing charges will almost certainly outperform someone who started earlier but scattered money across individual stocks with no strategy, high trading costs, and emotional decision-making.

We know this because that was us.

What we found

We started with Motley Fool. Not as a platform but as a source of direction. At the time, we had no framework at all. We did not know what a fund was. We did not understand the difference between an ETF and an investment trust. We did not know what an ongoing charge was or why it mattered. Motley Fool gave us a starting point and a set of ideas to test against everything else we read.

What it also gave us, unintentionally, was a bias toward picking individual stocks. That is not a criticism. It is what happened. We followed recommendations, bought shares in companies, and built a small portfolio of individual holdings that we checked far too often and understood far too little.

The turning point was not a single event. It was a slow realisation over about eighteen months that we were spending time and mental energy on something that was not working consistently, and that the people who seemed to be doing well over the long term were doing something much simpler.

They were buying broad index funds or ETFs. They were setting up a monthly direct debit. They were not checking the app every morning. They were not reacting to market news. They were not picking stocks. They were investing in the entire market, keeping costs low, and leaving it alone.

We shifted. Not overnight, but gradually. We sold the individual stocks, most at a small loss, a couple at a modest gain, and moved the money into a global index ETF inside a stocks and shares ISA. We set up a direct debit of what we could afford at the time, which was not much. And we stopped trying to be clever.

That shift changed everything. Not because the returns were immediately better. They were not. The first year was flat. But because the mental load disappeared. We were no longer researching individual companies, wondering whether to sell, wondering whether we had picked wrong. We had a plan that required almost nothing from us each month. Contribute, hold, ignore the noise.

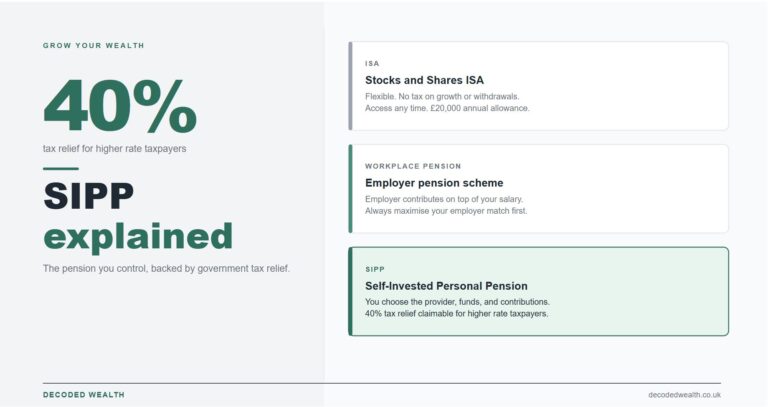

The plan we use now is simple enough to fit in two sentences. We invest monthly into broad global index funds inside a stocks and shares ISA, with a SIPP contribution alongside it for the tax relief. We wrote separately about how we split our money between ISA and SIPP if you want the detail on that. We review the allocation twice a year and otherwise leave it alone.

It took us too long to arrive at that. But arriving late turned out to be significantly better than not arriving at all.

What to do

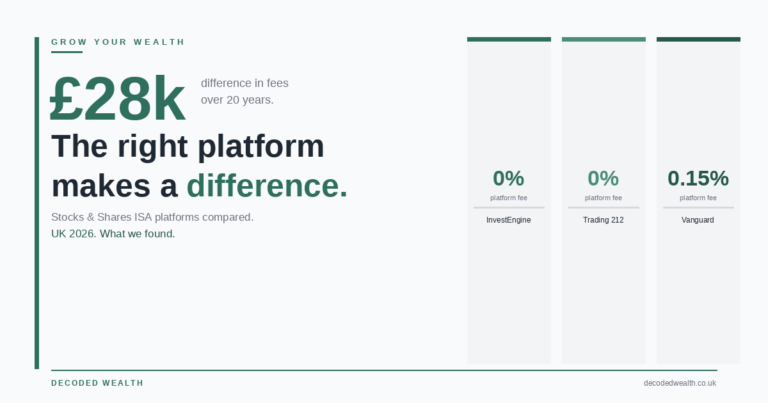

Step 1. Stop researching and open a stocks and shares ISA today. Not next week. Today. The account takes twenty minutes to set up. The annual ISA allowance is £20,000, and everything invested inside it grows free from income tax and capital gains tax. InvestEngine and Trading 212 both offer zero platform fee ISAs – Open an InvestEngine ISA or Open a Trading 212 ISA. IG offers a broader range if you want more flexibility – Open an IG Stocks and Shares ISA. The platform matters less than the act of opening it. We cover the main options in our ISA platforms comparison.

Step 2. Pick one fund. A single global index fund or ETF is a perfectly reasonable starting point. A Vanguard FTSE All-World ETF, an iShares MSCI World ETF, or an HSBC FTSE All-World Index fund. You do not need five funds. You do not need to diversify across fifteen holdings. One broad global fund gives you exposure to thousands of companies in a single purchase.

Step 3. Set up a monthly direct debit for whatever you can afford. If that is £50, it is £50. If it is £200, it is £200. The amount matters less than the consistency. You can increase it later when your income allows. What matters right now is that money moves from your bank account into your ISA every month without you having to think about it or decide each time.

Step 4. Do not buy individual stocks. Not yet. Maybe not ever. If you want to learn about individual companies later, after you have a core portfolio running on autopilot, you can allocate a small amount to that separately. But your first investment should not depend on your ability to pick winners. Broad index funds remove that pressure entirely.

Step 5. Accept that you will see red numbers. Your portfolio will go down at some point. It might go down in the first month. That is normal. A global index fund reflects the performance of thousands of companies across the world. It moves. Over any single year, it might drop 10%, 20%, or more. Over the long term, the historical trend has been upward, and we look at what staying out of the market actually costs over time in a separate article. The people who benefit from that long-term direction are the ones who stay invested through the drops, not the ones who sell when the number turns red.

Step 6. Review once a year. Check the fund, check the charges, consider whether to increase your contribution. Then close the app and get on with your life. The best investment strategy is one you can maintain for decades without it requiring your attention every week.

We did not start early. We did not start with much. We started badly, picked the wrong things, and spent months watching the numbers go down before we understood what we were doing. None of that turned out to matter as much as we thought it would at the time. What the maths penalises is not getting it wrong at first. It is not beginning at all.

Capital at risk. Investments can go down as well as up. This article is for informational purposes only and does not constitute financial advice. Decoded Wealth is not regulated by the FCA. Always do your own research before making financial decisions. This article may contain affiliate links. If you use them, we may earn a small commission at no extra cost to you.