How ISAs Actually Work (And How to Use Them Properly)

If you are in the UK and want to start saving or investing properly, you will keep hearing the same thing: use an ISA.

The problem is most people open one without really understanding what it is, which type to use, or where to actually put their money.

We made the same mistake at the start.

We now use a Stocks and Shares ISA with IG for flexibility, and Vanguard for our Junior ISA and pension. It took time to get to that setup.

This is the simple version of how ISAs actually work, and how we would set one up again from scratch.

What an ISA actually is

ISA stands for Individual Savings Account. The name is a bit misleading because it is not just for cash savings. It is a tax wrapper, a container that sits around your money and shields it from tax.

Anything that grows inside an ISA is free from income tax and capital gains tax. You never have to declare it on a tax return. The government does not get a cut of your returns. That is the whole point.

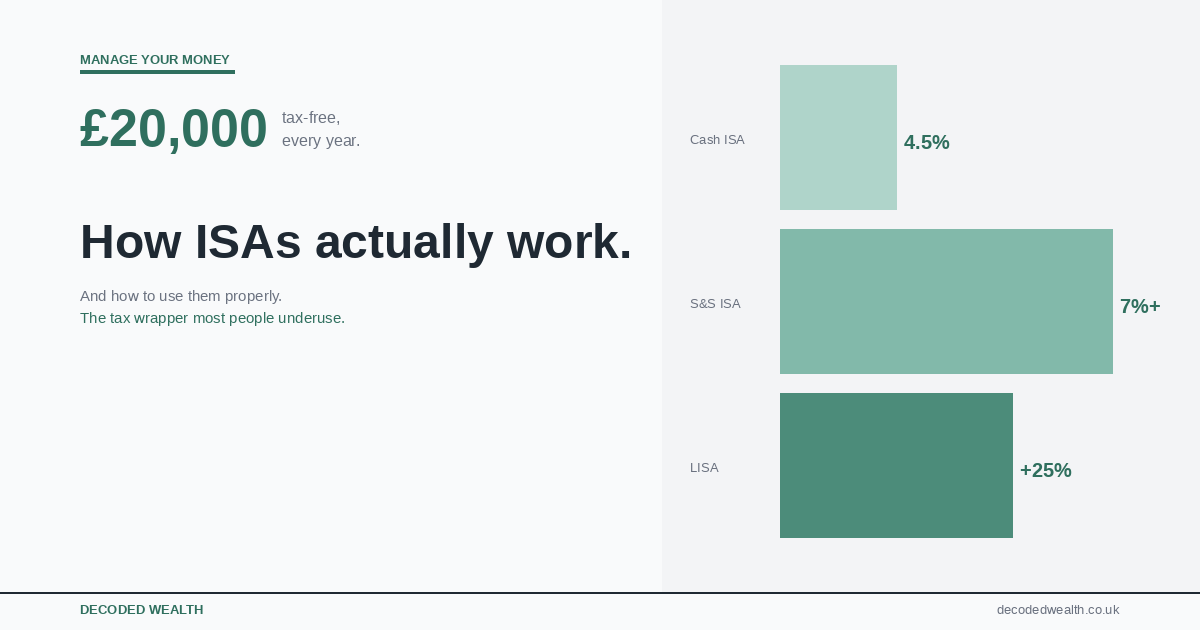

Each tax year you can put up to 20,000 pounds into ISAs. That is your annual allowance. If you do not use it, it is gone. You cannot carry it forward to the next year.

The different types of ISA

Cash ISA: This is just a savings account wrapped in an ISA. Your money sits in cash and earns interest, tax-free. Good for short-term goals or emergency funds. Not great for long-term wealth building because cash does not grow fast enough to beat inflation over decades. If you are thinking about how to build wealth properly, we break this down step by step here.

Stocks and Shares ISA: This is where you invest in funds, shares, ETFs, or investment trusts. Everything grows tax-free inside the wrapper. This is what we use for our own long-term investing.

Lifetime ISA (LISA): You can put in up to 4,000 pounds a year and the government adds a 25 percent bonus on top. Designed for first-time buyers or retirement. There are strict withdrawal rules so understand those before opening one.

Junior ISA (JISA): For children under 18. The allowance is 9,000 pounds a year for 2025/26. Money is locked until the child turns 18. We use this for our own children and explain our setup below.

Innovative Finance ISA: For peer-to-peer lending. Higher risk, more complex. Not where we would start.

What we would do if starting again

If we were starting from scratch today in the UK, this is how we would approach it.

If your goal is long-term investing, open a Stocks and Shares ISA.

Start simple. Pick a platform that is easy to use and low cost. Vanguard is a good option if you want something straightforward. IG works well if you want more flexibility and a wider range of investments.

Do not overcomplicate the investment choice. A global index fund or ETF is enough to begin with.

The most important thing is to get money invested consistently, not to pick the perfect fund.

Before investing, it also helps to have your money structured properly so you know what you can invest each month.

The tax benefit explained simply

Say you invest 10,000 pounds and it grows to 20,000 pounds over ten years. Outside an ISA, you could owe capital gains tax on the 10,000 pound profit when you sell. Inside an ISA, you owe nothing.

For dividends it is the same story. Outside an ISA you might pay income tax on dividends above your personal allowance. Inside, they are yours to keep.

Over decades, this tax-free compounding makes a real difference. It is not a small perk. It is one of the best things available to UK investors and most people do not use it anywhere near as much as they could.

How we use our ISAs: IG for the adult ISA

There is no single best ISA platform in the UK. It depends on how simple or flexible you want things to be.

We use IG for our Stocks and Shares ISA. We chose it for the breadth of what you can invest in, over 15,000 global shares, ETFs, and investment trusts, the fact it is a well-established FCA-regulated UK platform, and the flexibility of a flexible ISA which means you can take money out and put it back in the same tax year without losing your allowance.

Since 2026, IG has removed custody fees, which makes it more competitive for buy-and-hold investors like us. There is no commission on UK and US share trades, and the platform pays interest on uninvested cash while you decide what to buy.

One honest note: IG is not the most beginner-friendly platform. It is powerful and has a lot going on. If you want to explore how IG works, you can do that on their website, but if you want something simpler to start, platforms like Vanguard or Trading 212 are worth looking at.

Junior ISA: why we chose Vanguard

For our children’s Junior ISA, we went with Vanguard. The reason is simple: the JISA market in the UK is more limited, and for a long-term account where the money will sit for ten to eighteen years, we wanted the lowest possible fees and the least complexity.

Vanguard charges around 0.15 percent a year on Junior ISA balances. Importantly, the monthly minimum fee that applies to some adult accounts does not apply to JISAs. That keeps costs very low.

We picked a Vanguard LifeStrategy fund and left it alone. The fund automatically rebalances and covers global equities and bonds in one place. We did not want to pick individual stocks for our children’s account or spend time managing it actively.

Simple, cheap, and long-term is exactly what a Junior ISA should be.

Vanguard’s fund selection is narrower than IG, but for a JISA that is more than enough. You are not looking for hundreds of options. You want a small number of good ones.

We also use Vanguard for our SIPP for the same reason: low cost and simple long-term investing.

ETFs and investment trusts: why they work for beginners

Rather than buying shares in one company and putting all your eggs in one basket, ETFs and investment trusts spread your money across hundreds or thousands of companies in a single purchase.

An ETF tracking a global index might hold shares in 3,000 to 4,000 companies across dozens of countries. If one company struggles, it barely moves the overall value.

Investment trusts work similarly but are structured differently and can sometimes trade below the value of what they hold.

For most beginners, trying to pick individual stocks adds risk without much benefit early on. Broad funds do the heavy lifting for you.

The other advantage is cost. A broad global ETF might charge around 0.15 to 0.20 percent a year. Many actively managed funds charge significantly more. Over decades, that difference matters.

How to open a stocks and shares ISA in the UK: step by step

The process is similar across most platforms and takes about fifteen to twenty minutes.

- Choose your platform. Vanguard is simple and low cost. IG offers more flexibility. Trading 212 is fee-free and beginner-friendly. Compare based on fees, available investments, and ease of use.

- Go to the platform website and select to open a Stocks and Shares ISA.

- You will need your full name, home address, date of birth, and National Insurance number.

- Verify your identity. Usually a passport or driving licence. Some platforms do this instantly.

- Deposit money via bank transfer or debit card.

- Choose what to invest in. If you are not sure, a global index fund or ETF is a solid starting point.

- Set up a regular monthly payment if you can. Investing consistently matters more than timing the market.

That is it. You do not need to overthink this. The hardest part is starting.

If you are comparing options, we will break down the best ISA platforms in the UK in a separate guide.

A few things worth knowing

You can hold multiple ISAs: Since April 2024, you can pay into more than one Stocks and Shares ISA in the same tax year, as long as your total contributions stay within the 20,000 pound allowance.

Transfers do not use your allowance: Moving an old ISA to a new provider does not count as a new contribution.

The tax year matters: The UK tax year runs from 6 April to 5 April. Your allowance resets each year. Unused allowance does not carry forward.

Capital at risk. Investments can go down as well as up. This article is for informational purposes only and does not constitute financial advice. Decoded Wealth is not regulated by the FCA. Always do your own research before making financial decisions. This article may contain affiliate links. If you use them, we may earn a small commission at no extra cost to you.