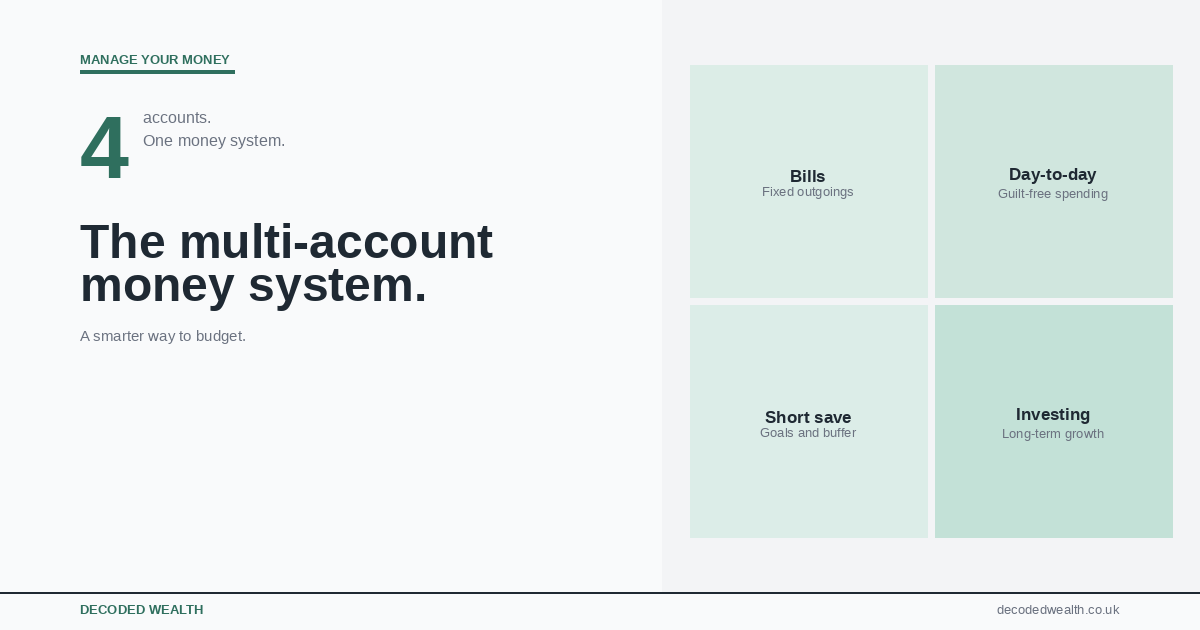

The Multi-Account Money System: A Smarter Way to Budget

Most people who try to budget fail. Most people who try to budget fail, not because they lack discipline, but because traditional budgeting relies on constant tracking and restraint. That isn’t a system. It’s willpower , and willpower runs outs out.

The smarter approach is to decide where your money goes before you spend a single pound. Every account has a job. Every transfer is automatic. By the time you spend, the allocation is already done.

This system is built on one principle: your fixed commitments come first, everything else follows. You do not start with a savings target and work backwards. You start with what you actually owe, account for how you actually live, and save and invest whatever is genuinely left.

The shift that changes everything Budgeting is reactive – you track what happened. Allocation is proactive – you decide what will happen. The difference is structural, not motivational.

A good structure beats good intentions every time.

Start here: the priority order

Before opening a single account or setting up any standing orders, understand the sequence. This is not a percentage split to aim for. It is a hierarchy – and the order is non-negotiable.

| Priority | Bucket | What goes here | How to calculate it |

| 1 | Fixed commitments | Mortgage or rent, nursery fees, car lease, council tax, utilities, insurance, phone | Add every direct debit to the penny. Add 10% buffer. This leaves first, every month, without exception. |

| 2 | Monthly life expenses | Food, transport, fuel, social spending, everyday costs | Average of your last three months of variable spending. Round up, not down. Not sure where to start? Our guide on how much to save each month gives you a realistic benchmark |

| 3 | Savings | Emergency fund first, then shorter-term goals – house deposit, car, planned career break | Until you have three to six months of expenses saved, everything goes here before anything goes to investing. |

| 4 | Investment | Stocks and shares ISA, pension top-ups, long-term wealth building | Once your emergency fund is in place, this runs as a standing order on payday alongside savings. |

| 5 | Holiday and travel fund | Holidays, weekends away, flights, hotels, spending money abroad | Two years of actual travel spend divided by 24. Funded from within your overall allocation, not on top of it. |

The holiday fund sits last in the hierarchy because it is calculated from real past spending – it is already embedded in how you live. Savings and investment are what you build deliberately once fixed costs and daily life are covered.

The five accounts – and what each one does

Each account has a single defined purpose. Money does not move between them freely. That separation is the mechanism that makes everything work.

| Account 1 – The bills account | Any basic current account |

| Every fixed direct debit. Nothing else. Your mortgage or rent, nursery fees, car lease, council tax, water, utilities, insurance, phone – every non-negotiable monthly commitment leaves from here. The debit card for this account is never used for discretionary spending. Calculate your total fixed direct debits, add a 10% buffer for anything that varies slightly, and transfer that amount on payday via standing order. The balance never drops below what is needed because nothing unexpected ever comes out of it. |

| Account 2 – The spending account | Monzo, Starling or any other basic account |

| Everyday life – food, transport, social, fuel. Funded by your honest estimate of monthly variable costs, not what you aspire to spend, but what you actually do based on the last three months. Once the transfer lands on payday, this money is yours to use without tracking every transaction. When it is gone, it is gone. That boundary is the point. Monzo and Starling work well here because their apps show your real-time balance clearly, so you always know where you stand without opening a spreadsheet. |

| Account 3 – The savings account | High-interest easy access account or cash ISA |

| Your financial foundation – emergency fund first, then savings goals. This receives its allocation on payday as a standing order, before any discretionary spending begins. If you do not yet have three to six months of expenses saved as an emergency fund, that comes first. A cash ISA is a sensible home if you have annual allowance remaining – interest is tax-free and the separation from your current account prevents casual dipping. Once the emergency fund is in place, this account shifts to shorter-term goals: a house deposit, a car, a planned career break. |

| Account 4 – The investment account | Stocks and shares ISA or pension |

| Long-term wealth – consistent, low-cost, left to compound. Once your emergency fund is established, part of what remains goes here on payday as a standing order. Not a fixed aspirational percentage, the actual amount left after your real costs are covered. Some months that is more, some months less. The habit of investing whatever is left, rather than spending it, is the structural change that builds wealth over time. A pension contribution benefits from tax relief on top; a stocks and shares ISA grows free of capital gains and income tax. |

| Account 5 – The holiday and travel account | Currency account |

| Holidays, weekends away, and all travel including foreign currency. Add up everything spent on travel and holidays over the last two years – flights, hotels, car hire, spending money, everything. Divide by 24. That monthly figure transfers here automatically. You are not saving for a specific trip, you are building a fund that reflects how you actually live, spread evenly across the year so it never feels like a lump sum you need to find at short notice. Currency account (like Revolut) handles foreign currency with no fees, so when you travel the money is in the right account and in the right currency. A lighter year means the surplus rolls forward. A heavier year means a conscious top-up, not a credit card. |

The credit card layer

A credit card, used correctly within this system, earns real rewards on spending you were going to do anyway, cashback, air miles, etc, without costing a penny in interest. The condition is simple: you only use the card on what is already allocated in one of your accounts, and the full balance clears automatically every month via direct debit from your bills account.

Choosing the right card, maximising rewards, and using credit strategically without risk is a topic worth covering properly, we will be doing exactly that in a dedicated article. If that is something you are thinking about, it is worth reading before you apply for anything.

| The one rule that cannot be bent If the money is not already sitting in your spending or travel account, it does not go on the credit card. The card is a payment method, never a borrowing facility. Set up a full balance direct debit on the payment due date and do not deviate from it. |

Working out your numbers: step by step

This takes about 30 minutes and only needs to be done properly once. Run through it before you set up any standing orders.

- List every fixed direct debit. Mortgage or rent, nursery fees, car lease, council tax, water, every utility, every insurance, phone, and any other commitment that leaves on a fixed date. Add them up exactly, then add 10% as a buffer. This is your bills account transfer.

- Estimate your monthly life expenses honestly. Look at three months of variable spending: food, transport, fuel, social, everyday costs. Take the average. Round up, not down. This funds your spending account.

- Calculate what is left. Subtract your bills total and your life expenses from your monthly take-home pay. That remainder is your savings and investment allocation. If it is smaller than you expected, the answer is in your fixed costs or spending habits, not in setting an aspirational savings figure that collapses in month two.

- Split the remainder between savings and investment. Until your emergency fund is in place, everything goes to savings. Once that foundation is built, divide it: savings for shorter-term goals, investments for long-term wealth.

- Calculate your holiday and travel monthly amount. Total everything spent on travel in the last two year: flights, hotels, spending money, the lot. Divide by 24. This is your Revolut transfer. It accounts for both heavy and light years and removes the need to find a lump sum when a trip comes around.

On honesty The numbers only work if they reflect reality. Underestimating food costs or forgetting a subscription does not make the system work better – it makes your spending account run dry and you start borrowing from other buckets. An uncomfortable accurate number is more useful than a comfortable wrong one

Setting it up

- Open a dedicated account for each purpose. Most are free and take under 10 minutes online.

- Run the calculation sequence above before setting up any standing orders.

- Set up standing orders from your main account on payday, one transfer per account, automated, done once.

- Set your currency account for travel and fund it only from your holiday allocation, never from your spending account.

- Set a full balance direct debit on your credit card from your bills account, due date, every month.

- Review the whole system every six months, or immediately after a significant change, a pay rise, a new fixed commitment, a child starting school.

| Start with three if five feels like too much: Bills, spending, and savings. Get those running smoothly first. Add the investment account once your emergency fund is established, and the holiday account when the rest is in place. The system works at any level of complexity, it does not need to be complete on day one. |

Common questions

What if my fixed costs leave almost nothing for savings?

Then your fixed cost base is high relative to your income, and the priority is reducing it over time, a mortgage review, a lease that ends, nursery fees that will eventually stop. In the meantime, even a small savings transfer matters. It builds the habit. Fifty pounds a month saved consistently beats three hundred saved erratically when you happen to feel flush.

What if one of my two travel years was unusually expensive?

Use your judgement. If one year included a once-in-a-decade trip that distorts the average, weight toward the more typical year. The goal is a monthly figure that reflects how you genuinely live, not an outlier. You can adjust the Revolut transfer mid-year if your plans change significantly.

Does this work with irregular income?

Yes, with one adjustment. Rather than standing orders on a fixed date, run the allocation manually each time you are paid using the same sequence. Some people with variable income find it useful to work in percentages of each payment rather than fixed amounts – that way a quieter month automatically produces proportionally smaller transfers to each bucket.

What if my spending account runs out before the end of the month?

The system is working. It is telling you either that the allocation was set too low and needs adjusting, or that spending ran higher than usual this month. In the first few months, most people make one or two small adjustments before it stabilises. The key is not to borrow from another account – that defeats the separation and starts a habit of treating all money as interchangeable, which is exactly what this system is designed to prevent.

How often should I review the allocations?

Every six months as a minimum, and immediately after any significant change to income or fixed costs. A pay rise is a natural trigger to increase savings and investment allocations before lifestyle spending expands to fill the gap. A new fixed commitment means recalculating from step one.

If you have not yet worked out how much you should be saving each month, read this first : Are you saving enough? The UK reality check

Decoded Wealth is an independent personal finance blog. Nothing here constitutes regulated financial advice. Credit card eligibility depends on your individual circumstances. Always clear your full balance each month to avoid interest charges. Capital at risk where investments are mentioned.