Salary Sacrifice and the £100k Childcare Trap

For several years we paid income tax and National Insurance on things we could have obtained with pre-tax money. Not because the schemes were unavailable. We simply had not looked at what our employers offered.

When we finally did, it was not the car scheme or the bike that made us act. It was nursery fees. We wanted to protect the 30 hours free childcare entitlement and access Tax-Free Childcare. Salary sacrifice was the mechanism that kept both. Once we understood that, we started paying attention to everything else it could do.

What most people do wrong

Most people use salary sacrifice for pension only, if they use it at all. Some do not even realise their employer’s pension contributions involve salary sacrifice by default.

That is not the mistake. The mistake is stopping there.

Salary sacrifice extends to electric vehicles, cycles, and in some cases additional annual leave, mobile phones, and professional subscriptions. Each scheme works on the same principle: your gross salary is reduced by the cost of the benefit, and you pay tax and National Insurance only on the reduced salary.

For a higher rate taxpayer, the relief applies at 40%. That changes the value of every scheme significantly compared to basic rate.

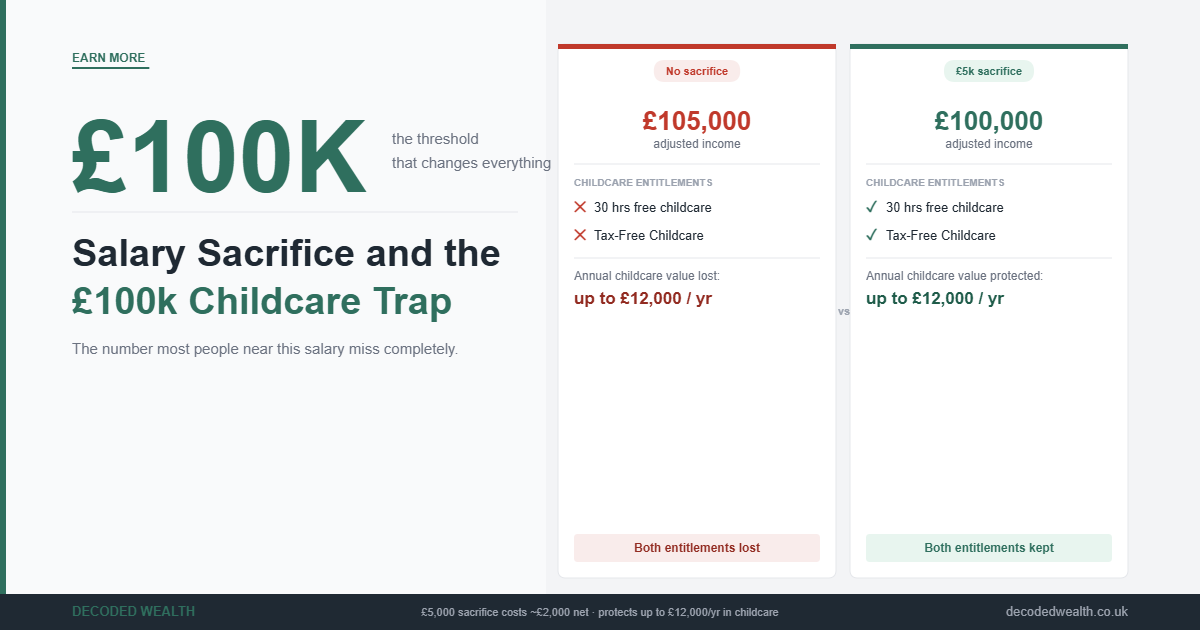

For anyone with young children earning near £100,000, the stakes are higher still. Both the 30 hours free childcare and Tax-Free Childcare require each parent’s adjusted net income to stay below £100,000. Salary sacrifice pension contributions reduce adjusted net income directly. The decision to sacrifice or not at this salary level is not just about tax efficiency. It is about whether your family keeps access to childcare support worth thousands of pounds a year.

We know families who did not run this calculation. They earned just above £100,000, did not use pension sacrifice, and lost both entitlements. The nursery bill was not covered by the additional salary above the threshold. They were materially worse off for earning more.

What is actually happening

Your employer reduces your contractual salary by the value of the benefit. Your employer does not tax that reduction. Your take-home pay reflects the lower gross, and the employer provides the benefit in lieu.

The saving comes from two places: income tax at your marginal rate, and National Insurance at 12% or 2% depending on where your salary sits. Your employer also saves National Insurance at 13.8% on the sacrificed amount. Some employers pass part of that saving back to you, which makes the scheme more favourable than the headline figures suggest.

The childcare threshold.

The 30 hours free childcare gives working parents of three and four year olds 30 funded hours per week during term time, across 38 weeks per year. At average UK nursery rates, that is worth between £6,000 and £10,000 per year per child. In London and the South East, more.

Tax-Free Childcare adds a 20% government top-up on money paid into a childcare account. That is worth up to £2,000 per year per child, or £4,000 for a disabled child.

Combined, these two schemes can be worth £8,000 to £12,000 per year per child. They disappear entirely the moment either parent’s adjusted net income exceeds £100,000.

The maths between £100,000 and £125,140 is stark for any family with young children. A £5,000 pension sacrifice costs £2,000 net at the 60% effective rate in that band. The childcare entitlements it protects are worth multiples of that. No other decision at this income level produces a comparable return.

| Salary | Pension Sacrifice | Adjusted Net Income | Childcare Eligibility |

|---|---|---|---|

| £105,000 | £0 | £105,000 | Lost |

| £105,000 | £5,000 | £100,000 | Kept |

Electric vehicles.

The benefit in kind (BiK) tax rate on fully electric vehicles is 2% in 2025/26, rising to 3% in 2026/27 and incrementally thereafter. On a £40,000 electric vehicle through salary sacrifice, the gross monthly sacrifice is around £650. A higher rate taxpayer saves income tax at 40% on that amount, plus NI at 2%.

Including the BiK tax, the net monthly cost sits in the region of £390 to £420. The same car leased personally would cost considerably more. For anyone near the point of changing their car, the numbers are difficult to ignore.

Cycle to work.

The scheme allows employees to sacrifice salary for a bike and equipment up to £3,500. For a higher rate taxpayer, a £1,000 package costs approximately £580 net after tax and NI savings. The employer owns the bike during the hire period and transfers it to the employee at the end, typically for a small final payment.

Pension contributions.

Salary sacrifice pension contributions save both income tax and National Insurance. Personal pension contributions save only income tax. On a higher rate salary, that difference compounds materially over years. For anyone near the £100,000 threshold, pension sacrifice also reduces adjusted net income. That is the mechanism that protects childcare eligibility.

What we found

When we worked through the EV scheme properly, the saving was larger than we had assumed. The combination of income tax, National Insurance, and the low BiK rate on electric vehicles makes this one of the most efficient ways to run a car for employees whose employers offer it.

The childcare calculation was the more significant finding. Once we modelled what losing the 30 hours and Tax-Free Childcare would actually cost, and how little pension sacrifice it took to stay below the threshold, the decision was straightforward. The question was only why we had taken so long to look at it properly.

We also found that the schemes are not available everywhere. Some employers offer only pension sacrifice. Others offer a full suite of benefits. The only way to know is to ask HR or check the employee benefits portal directly.

One thing worth checking before committing: reducing your gross salary reduces your pensionable pay under some schemes, which can affect defined benefit pension accrual. It may also reduce the income figure a mortgage lender uses for affordability. Neither is a reason not to use the schemes, but both are worth understanding before you sign anything.

What to do

Step 1. If either partner earns near £100,000, run the childcare calculation first.

Check your adjusted net income. If it is above £100,000 or close to it, model what pension sacrifice would cost versus what childcare entitlements it protects. For most families with young children, that calculation takes ten minutes. The answer is usually the same: the sacrifice costs less than the entitlements are worth.

Step 2. Find out what schemes your employer offers.

Ask HR or check your employee benefits platform. Do not assume the answer is only pension. Many employers offer EV, cycle to work, and other schemes that most employees have never looked at.

Step 3. Calculate the net cost for any scheme you are considering.

Take the gross monthly sacrifice. Apply your marginal income tax rate and NI. Add back any BiK tax for EVs. That gives you the real monthly net cost. Compare it to what the same item would cost if you purchased or leased it personally after tax.

Step 4. Check whether your employer passes on their NI saving.

Some employers apply their 13.8% NI saving to reduce the gross sacrifice further. Ask specifically. Not all volunteer this.

Step 5. Check the implications for your mortgage or pension before committing.

A lower gross salary may affect mortgage affordability calculations during the contract period. If you are in a defined benefit pension scheme, check whether the reduced salary affects your accrual. Both are manageable, but worth knowing upfront.

Step 6. Act on the EV scheme before the BiK rate rises.

The 2% BiK rate on electric vehicles increases year by year. Schemes entered now lock in the current vehicle price and lease terms for the duration of the contract. Waiting reduces the saving each year the BiK rate rises.

Most employee benefits platforms contain more value than most employees ever use. The salary sacrifice schemes are not complicated. They are invisible until someone shows you the numbers. Once you have seen them, it is difficult to justify not using them.

Capital at risk. Investments can go down as well as up. This article is for informational purposes only and does not constitute financial advice. Decoded Wealth is not regulated by the FCA. Always do your own research before making financial decisions. This article may contain affiliate links. If you use them, we may earn a small commission at no extra cost to you.