How Much Do You Need to Retire in the UK? The Numbers Most People Get Wrong

Most people avoid this question for one simple reason: they are afraid of the answer.

We were the same. Which, as strategies go, is not a great one.

It felt too big, too far away, and too easy to ignore.

When we finally sat down and worked through it properly, it was actually less terrifying than we expected. Because once you have a real number to aim for, the next question becomes what do I need to do each month to get there, and that is a much more tractable problem.

Here is the framework we use, in plain terms.

In this guide, we will show you:

- What retirement actually costs in the UK

- How much the State Pension reduces your target

- The simple formula to calculate your number

- What different pension pots give you in real terms

Start with what you actually need to spend

The Pensions and Lifetime Savings Association publishes annual retirement living standards for the UK. For 2024/25, they estimate that a single person needs around 14,400 pounds a year for a minimum standard of living, around 31,300 pounds for a moderate one, and around 43,100 pounds for a comfortable one. For couples those figures rise to roughly 22,400, 43,100, and 59,000 pounds respectively.

These are national averages and your number will be different. If you live in London or the South East your costs are higher. If you plan to travel regularly, higher again. If you own your home outright and have no mortgage by the time you retire, your monthly outgoings are significantly lower than someone still renting.

The starting point is working out what your retirement actually needs to cost. Not a fantasy version, not a stripped-back survival version. A realistic picture of the life you want. Write down the monthly costs. Be honest rather than optimistic.

The State Pension reduces the number significantly

The full new State Pension in 2025/26 is 11,502 pounds a year. To get the full amount you need 35 qualifying years of National Insurance contributions. You can check your personal forecast, it takes about five minutes. We would genuinely recommend doing it.

This matters a lot because it reduces how much your private pension and investments need to generate. If you need 31,000 pounds a year in retirement and the State Pension covers 11,500 of it, your portfolio only needs to produce around 19,500 pounds a year on top of that. That is a very different and more manageable target than 31,000.

Do not assume you will automatically receive the full amount. Career breaks, time spent self-employed, or years spent abroad can reduce your entitlement. And do not assume the rules will stay the same. The State Pension age has already risen to 67 and is due to rise again. Factor in some flexibility.

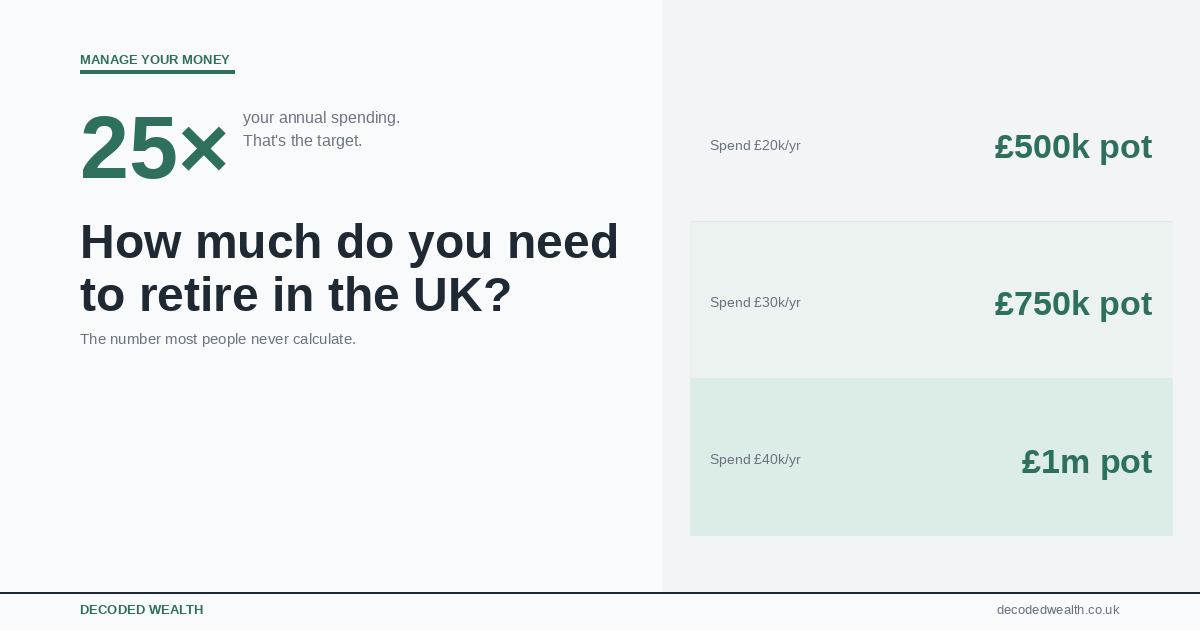

The 25 times rule: simple and useful

The most widely used rule of thumb in retirement planning is this: you need a pot worth 25 times your annual spending from investments to retire sustainably. This is because you can withdraw 4 percent of your pot each year and, if it is invested sensibly, the pot should last indefinitely.

The maths in practice: if your portfolio needs to generate 19,500 pounds a year on top of the State Pension, you need a pot of roughly 487,500 pounds. If you need 25,000 a year from your portfolio, you need around 625,000 pounds.

The 4 percent rule has been debated and refined over the years and is not a guarantee. But as a planning anchor it is useful, widely used, and gives you a real number to work with rather than a vague aspiration.

What different pot sizes actually get you in practice

300,000 pound pot: Generates around 12,000 pounds a year at 4 percent. Add the full State Pension and a single person has roughly 23,500 pounds a year. Modest but workable if the mortgage is paid off and costs are under control.

500,000 pound pot: Generates around 20,000 pounds a year. Add the State Pension and you are at around 31,500 pounds. This sits in the moderate retirement living standard and is a realistic target for many people who start saving seriously in their 30s.

750,000 pound pot: Generates around 30,000 pounds a year. With the State Pension, a single person has over 41,000 pounds. A couple with two State Pensions and a combined pot of this size is genuinely comfortable in most parts of the UK.

1,000,000 pound pot: Generates around 40,000 pounds a year. With the State Pension on top, this covers a comfortable retirement for most people in most parts of the country. This feels like a lot and it is. But for a couple, split across two pensions built over a full career with employer contributions and tax relief, it is more achievable than it sounds.

Working backwards to a monthly number

Once you have a rough pot target, the next question is what you need to save each month to get there. The government’s MoneyHelper service has a pension calculator that lets you input your age, current pension value, target age, and desired pot, and gives you a monthly contribution figure. Use it. The numbers tend to feel more manageable when they are broken down.

A rough illustration to give you a sense of scale: someone aged 35 with nothing currently saved wanting a 500,000 pound pot by 65 would need to contribute around 500 to 600 pounds a month into a pension, assuming 6 to 7 percent average annual growth. That includes the automatic 20 percent tax relief added by the government on basic rate contributions. For a higher rate taxpayer the effective cost is lower still.

That is not a small amount. But it includes everything your employer is matching, which at most workplaces adds at least a few percent on top of your own contribution for free.

The things that change the numbers most

Starting earlier: The single most powerful lever. Someone starting pension contributions at 25 needs to save roughly half as much each month as someone starting at 40 to reach the same pot. Time and compound growth do most of the heavy lifting if you give them enough runway.

Employer contributions: This is money you have earned but only receive if you contribute enough to trigger it. Maximising your employer match is always the first step, always, before any other savings or investment decision.

Tax relief: Basic rate taxpayers get 20 percent relief. Higher rate taxpayers get 40 percent. Every 60 pounds you contribute costs a 40 percent taxpayer 60 pounds in take-home but goes in as 100 pounds. That is a 67 percent instant return before the market does anything.

Owning your home by retirement: Retiring without a mortgage or rent to pay changes the annual income you need dramatically. Someone renting in retirement needs a significantly larger pot than someone who owns outright.

Work it out now, even if the number is uncomfortable

The biggest mistake people make is putting this calculation off because they are worried about what they will find. We did it ourselves and we understand the impulse.

But knowing you are behind is always better than not knowing. You cannot adjust course if you do not know you are off it. And the earlier you run the numbers, the more time you have to do something about them.

Your pension fits into a broader picture of how you build wealth over time. If you want to understand where it sits relative to your other financial priorities, our seven-step wealth-building order walks through the full sequence clearly.

Capital at risk. Investments can go down as well as up. This article is for informational purposes only and does not constitute financial advice. Decoded Wealth is not regulated by the FCA. Always do your own research before making financial decisions. This article may contain affiliate links. If you use them, we may earn a small commission at no extra cost to you.