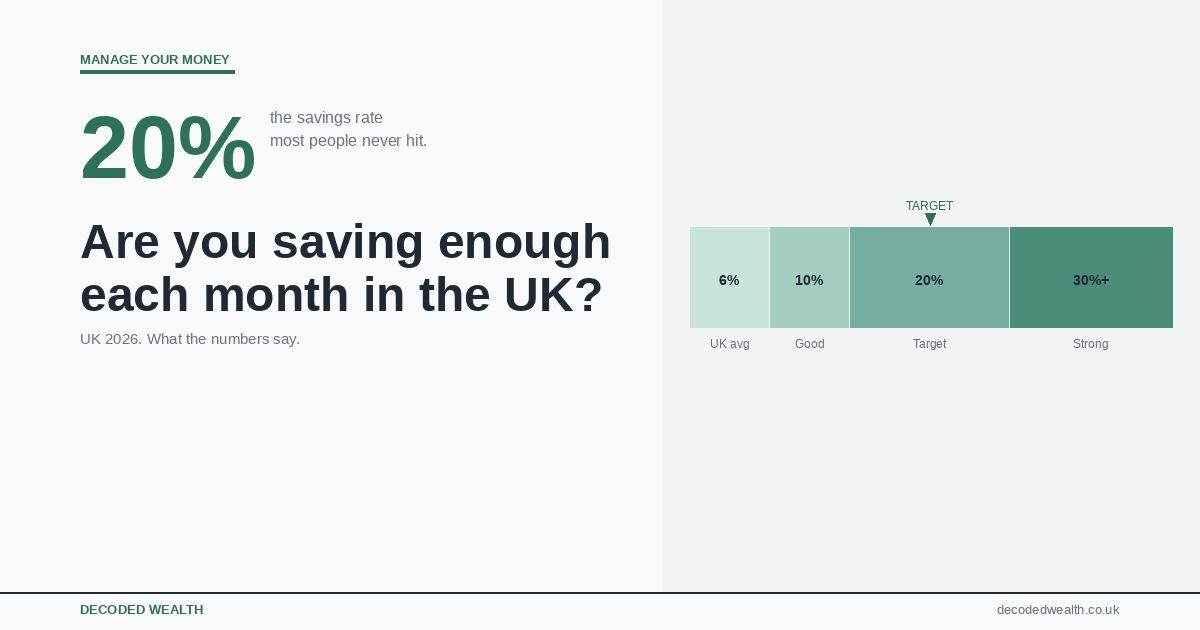

Are you saving enough each month in the UK (2026)?

The honest answer -with real 2026 data on what UK households are actually doing

This is one of those questions that sounds simple but quickly becomes complicated.

Ask a financial adviser and you will get a percentage. Ask your parents and they will probably say save as much as you can. Look online and you will find rules that were designed for American households twenty years ago and do not always reflect real life in the UK today.

The honest answer is that there is no single right number. But there are some useful benchmarks and a few habits that make a real difference. That is what this article covers.

What people in the UK are actually saving in 2026

It helps to start with what is actually happening, not what financial guides say should be happening.

The average UK adult is saving £288 a month in 2026, up from £226 the year before. But the median – the point where half of people save more and half save less – sits closer to £180 a month.

That gap between the average and the median matters. A relatively small number of higher earners saving large amounts pulls the average up considerably. For most households, £180 is a more realistic reference point.

The broader picture is striking. According to 2026 Finder data, 2 in 5 UK adults have £1,000 or less in savings. A quarter have £200 or less. And around 16% have nothing saved at all.

This is not about judgment. Housing costs, stagnant wages in some sectors, and the general cost of living in the UK make saving genuinely difficult for a lot of households. The point is simply that if you are saving something consistently – even if it feels modest – you are already ahead of a significant portion of the population.

Why the standard rules do not always work

You have probably heard the 20% rule. Save 20% of your take-home pay, spend 50% on needs, use 30% for everything else. It is clean, memorable, and repeated endlessly in personal finance content.

The problem is that it was written for a different housing market in a different country. For anyone renting in London, Bristol, Manchester or Edinburgh, housing alone can take 40 to 60% of take-home pay before a single other bill is paid. The 20% savings target, in that context, is aspirational at best.

So rather than chasing a percentage that does not fit your actual life, there is a more grounded approach.

Saving a smaller amount consistently is worth far more than setting an ambitious target and abandoning it after three months. A standing order for £50 a month that runs for five years beats a plan to save £500 a month that lasts six weeks.

A practical way to work out your own number

Instead of starting with a target percentage, work backwards from your actual situation.

- Add up your fixed essential monthly costs – rent or mortgage, utilities, food, transport, minimum debt payments.

- Decide what you can realistically move into savings every month without stretching yourself. Be honest, not aspirational.

- Set up an automatic standing order for that amount to leave your account on payday – before you see it or have a chance to spend it.

- Whatever is left in your account after that is yours to use freely. No tracking, no guilt, no spreadsheet.

The automation is the critical part. When saving happens automatically the moment your salary lands, it stops feeling like a sacrifice. The money never feels available to spend in the first place.

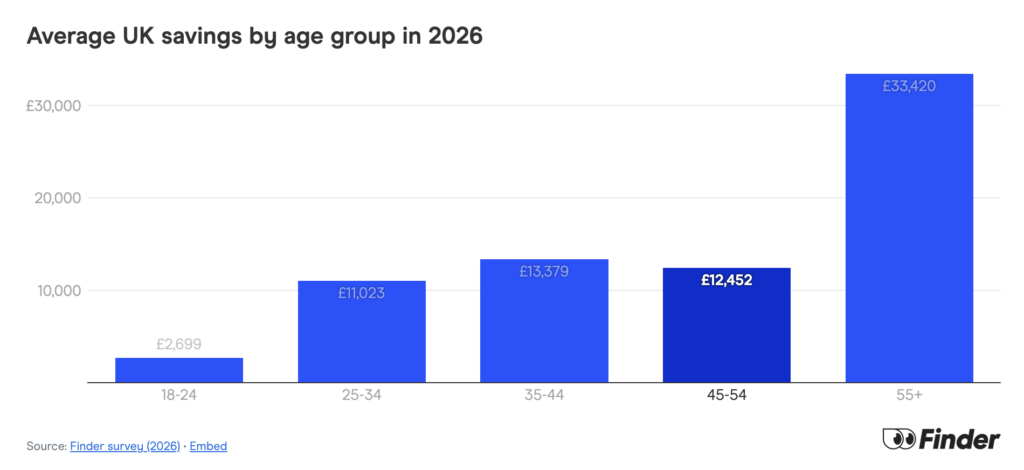

How savings tend to change through your 30s and 40s

Savings are not the same at every stage of life, and the data reflects this.

The average savings pot for 25 to 44 year olds in the UK currently sits at around £11,000. For the over 55s, it rises to £33,420. People in their 20s and 30s often have high savings ambitions but relatively modest actual pots – the gap between aspiration and reality is widest in this age group.

If you are in your 30s and feel behind, you are almost certainly closer to average than you think. The important thing is not matching a specific number – it is building a consistent habit that compounds significantly over the next two or three decades.

Starting a decade earlier makes a larger difference than saving a larger amount later. This is one of the few areas in personal finance where the cliche is genuinely true.

Where your savings should go – the priority order

If you are deciding where to put a limited amount each month, the order genuinely matters.

1) get your full employer pension match

If your employer matches pension contributions, make sure you are contributing at least enough to get the full amount. This is as close as personal finance gets to a guaranteed return – free money, plus tax relief on top.

2) build an emergency fund

Before investing, have some accessible savings for unexpected costs. Three months of essential expenses is the standard target. Without this buffer, a single unexpected bill can derail everything else.

3) clear expensive debt

Any debt above roughly 5% interest is usually worth clearing before investing. The guaranteed return from eliminating that debt typically beats what investments are likely to produce.

4) put the rest into your ISA

Once the above are in order, direct remaining savings into a stocks and shares ISA where they can grow tax-free over the long term.

The order matters as much as the amount. Following this sequence means every pound you save is doing the most efficient job it possibly can.

What consistent saving actually produces

This is where compound growth goes from abstract to genuinely motivating.

| Monthly saving | Starting age | Average return | Value at 65 |

| £100/month | Age 25 | 6% per year | ~£195,000 |

| £200/month | Age 25 | 6% per year | ~£390,000 |

| £300/month | Age 25 | 6% per year | ~£585,000 |

| £200/month | Age 35 | 6% per year | ~£195,000 |

Look at the last two rows. Someone saving £200 a month from age 25 ends up with twice as much as someone saving the same amount from age 35. The amount saved is identical. The only difference is ten years of time.

Time is the variable that matters most in personal finance. Not the platform, not the fund selection, not the exact percentage. Time.

The one habit that makes everything easier

For most people, the biggest practical shift is not saving more. It is making saving automatic.

When money leaves your account on the day your salary arrives, before you have had a chance to spend it, saving stops feeling like a sacrifice. The money never felt available in the first place.

If you do one thing after reading this article, make it this: set up a standing order to move money into a savings account on payday. Even £50 a month. Even £30. The habit is what matters at the start, not the amount.

The amount can increase later. The habit is what has to be established first.

What if saving is not realistic right now

It is worth being straightforward about this, because a lot of personal finance content glosses over it.

If your income is fully taken up by essential costs, meaningful saving is not always possible — and it is not helpful to pretend otherwise. Suggesting you cut out coffee when you cannot cover your rent is not advice.

In that situation, the most useful steps are usually: identifying whether any fixed cost can be reduced, looking at whether income can be increased even slightly, and setting up a very small automatic transfer – even £5 or £10 a month – purely to build the habit and keep the account structure in place for when things improve.

Frequently asked questions

How much should I save each month in the UK?

There is no fixed answer, but the median UK household saves around £180 per month in 2026. The most important thing is saving consistently rather than hitting a specific target.

Is saving 20% of income realistic?

For many people, especially renters in cities, it is not. A smaller consistent amount is more valuable than an ambitious target that does not stick.

What is a good amount to have saved?

A common starting point is three months of essential expenses as an emergency fund. Beyond that, the right amount depends on your goals, age, and situation.

Should I save or invest first?

Most people are better off building an accessible emergency fund first. After that, investing through a stocks and shares ISA is usually the most tax-efficient long-term approach.

Am I behind on savings for my age?

Probably not. The average savings pot for 25 to 44 year olds in the UK is around £11,000. Savings levels vary enormously and most people feel further behind than they actually are. Consistency over time matters more than comparing yourself to an average.

This article is for informational purposes only and does not constitute financial advice. Always do your own research before making any financial decisions.