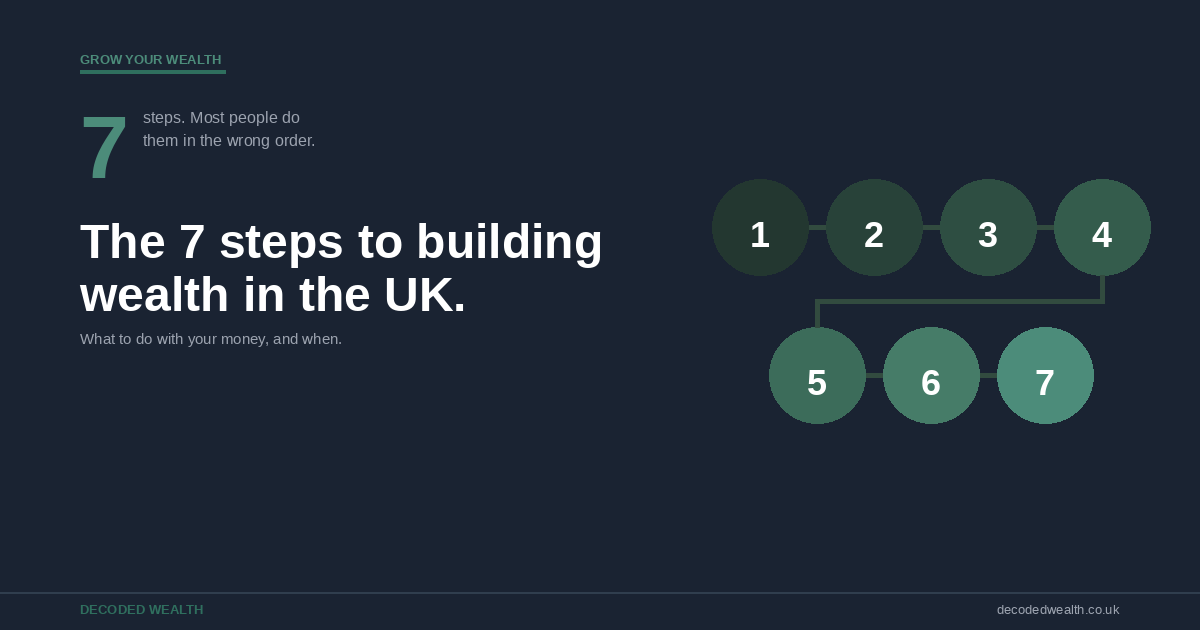

The 7 Steps to Building Wealth in the UK (What to Do With Your Money)

One of the most common questions we see is some version of this: I have a bit of money spare each month. What do I do with it first?

It is a great question, and the honest answer is that most people try to figure it out alone, end up overwhelmed by conflicting advice online, and either do nothing or do things in the wrong order.

Most people are not doing the wrong things. They are just doing them in the wrong order.

There is a rough order that makes sense for most people in the UK. It is not perfect for every situation, but it gives you a framework. Think of it as a set of steps you move through as your finances improve. You do not need to skip ahead, and you do not need to do everything at once.

This is roughly the order we follow ourselves, and we think it is a decent starting point for most people.

Step 1: Sort your baseline first

Before anything else, you need to know what is actually going on with your money. That means understanding what comes in, what goes out, and whether those two numbers leave you with anything.

If your spending is consistently more than your income, investing will not save you. The first job is to fix the gap. That might mean cutting some costs, it might mean finding ways to bring more in, or usually both.

You do not need a complex budgeting system. A simple spreadsheet or a free app like Monzo or Emma will do it. The goal is just to know your numbers.

If you are still working on step one, start with our guide to structuring your money properly.

Step 2: Build a small emergency fund

Before you pay off debt aggressively or invest, build a small cash buffer. We would start with one to three months of essential expenses. Three months is a solid target, but even one month puts you in a much stronger position than most people.

The reason this comes first is psychological as much as practical. Without a buffer, the first unexpected expense, a car repair, a boiler, a dental bill, forces you back into debt or forces you to sell investments at the wrong time.

In the UK right now, easy-access savings accounts are paying reasonable rates. Shop around, use a comparison site, and make sure your money is not just sitting in a current account earning nothing.

Step 3: Clear high-interest debt

If you have credit card debt, store card debt, or any loan above roughly eight to ten percent interest, paying that off is the best risk-free return you can get anywhere.

Think about it this way: paying off a credit card charging 20 percent interest is the equivalent of a guaranteed 20 percent return. No investment reliably gives you that.

The exception is low-rate debt like a mortgage or a 0 percent interest deal you are managing carefully. Those do not need to be rushed.

Student loan debt in the UK works differently to everywhere else. For most people, it functions more like a graduate tax than a traditional debt. We would not prioritise paying it off early above other steps, but it is worth understanding how your plan and threshold affect your repayments.

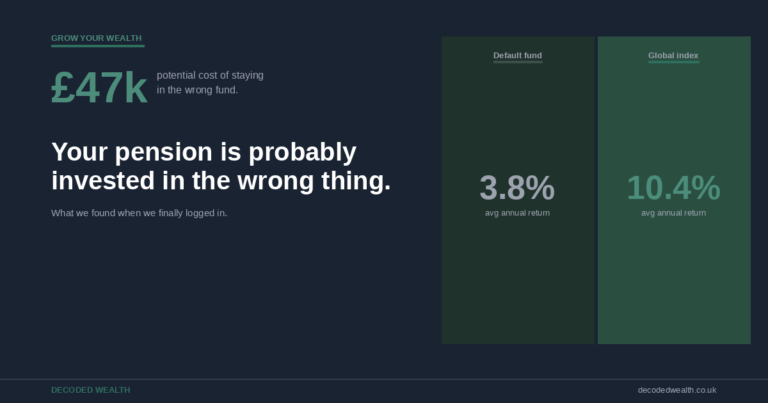

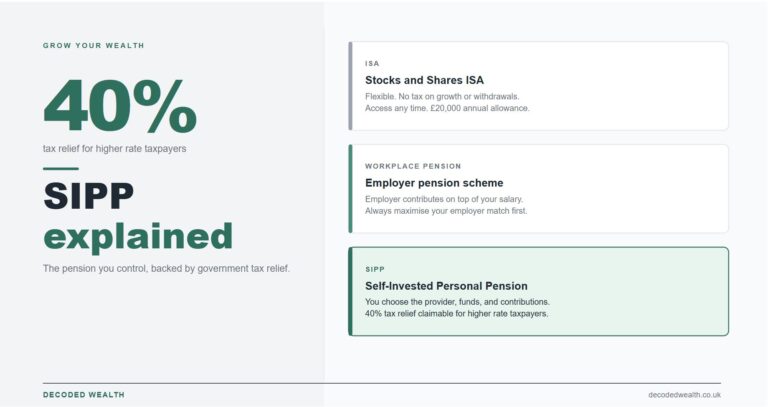

Step 4: Get your pension contributions right

Your workplace pension is one of the most valuable things available to you, and most people do not pay enough attention to it.

The basic rule: at minimum, contribute enough to get your full employer match. If your employer will match up to five percent of your salary, contribute at least five percent. Anything less and you are turning down free money. That is the simplest piece of financial advice that exists.

Beyond the match, pension contributions come with tax relief. If you are a basic rate taxpayer, every 80 pounds you put in costs you 80 pounds but goes in as 100 pounds with the government topping it up. For higher rate taxpayers the benefit is even greater.

The downside of pensions is that you cannot touch the money until you are 57 (rising to 57 in 2028). That is the trade-off. Great for retirement, useless if you need the money in five years.

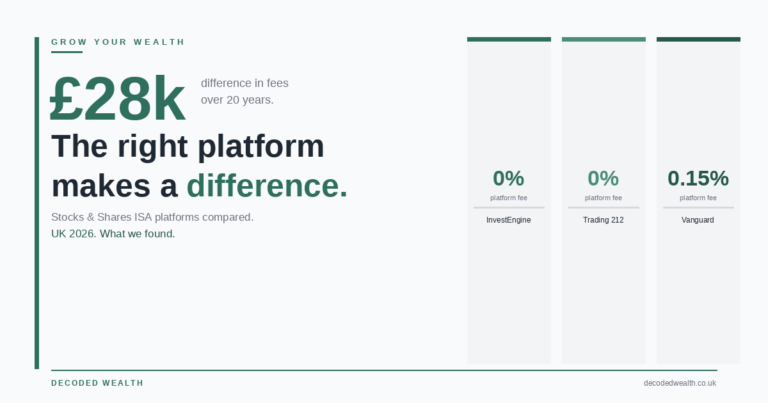

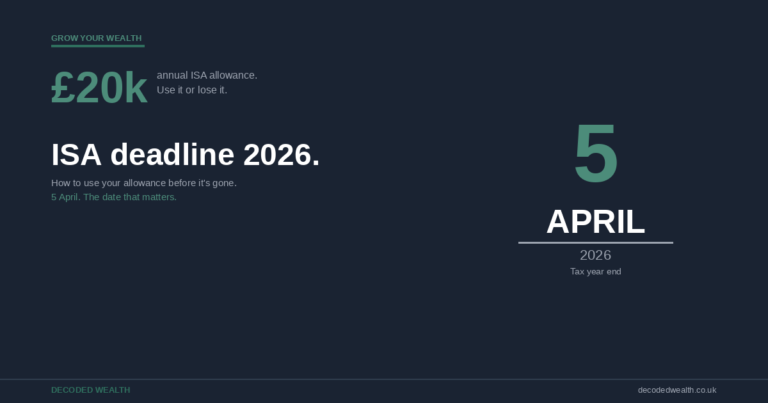

Step 5: Use your ISA allowance

Once your pension contributions are sensible and your emergency fund is in place, the ISA is the next place to put money.

You have an annual ISA allowance of 20,000 pounds per tax year. Anything that grows inside the ISA is free of income tax and capital gains tax, forever. It is the UK’s best tax wrapper for most people.

There are a few types worth knowing:

- Stocks and shares ISA: for investing in funds, shares, ETFs. Best for long-term wealth building.

- Cash ISA: for saving in cash with tax-free interest. Useful if you are saving for something specific within five years.

- Lifetime ISA: for first-time buyers or retirement. The government adds a 25 percent bonus on up to 4,000 pounds per year. Excellent if you qualify. There are penalties for withdrawing it for other purposes, so understand the rules first.

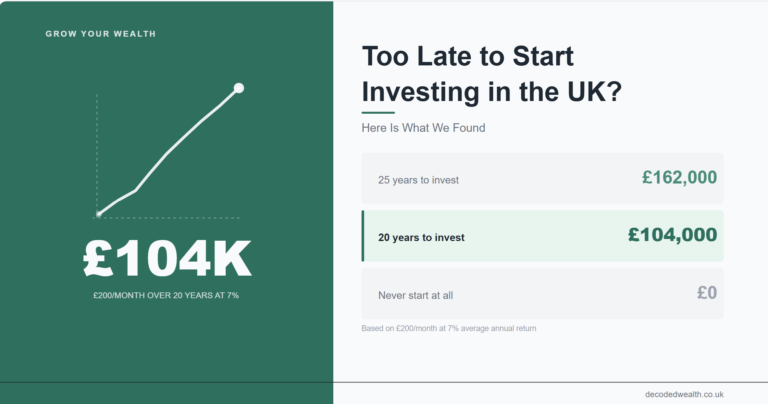

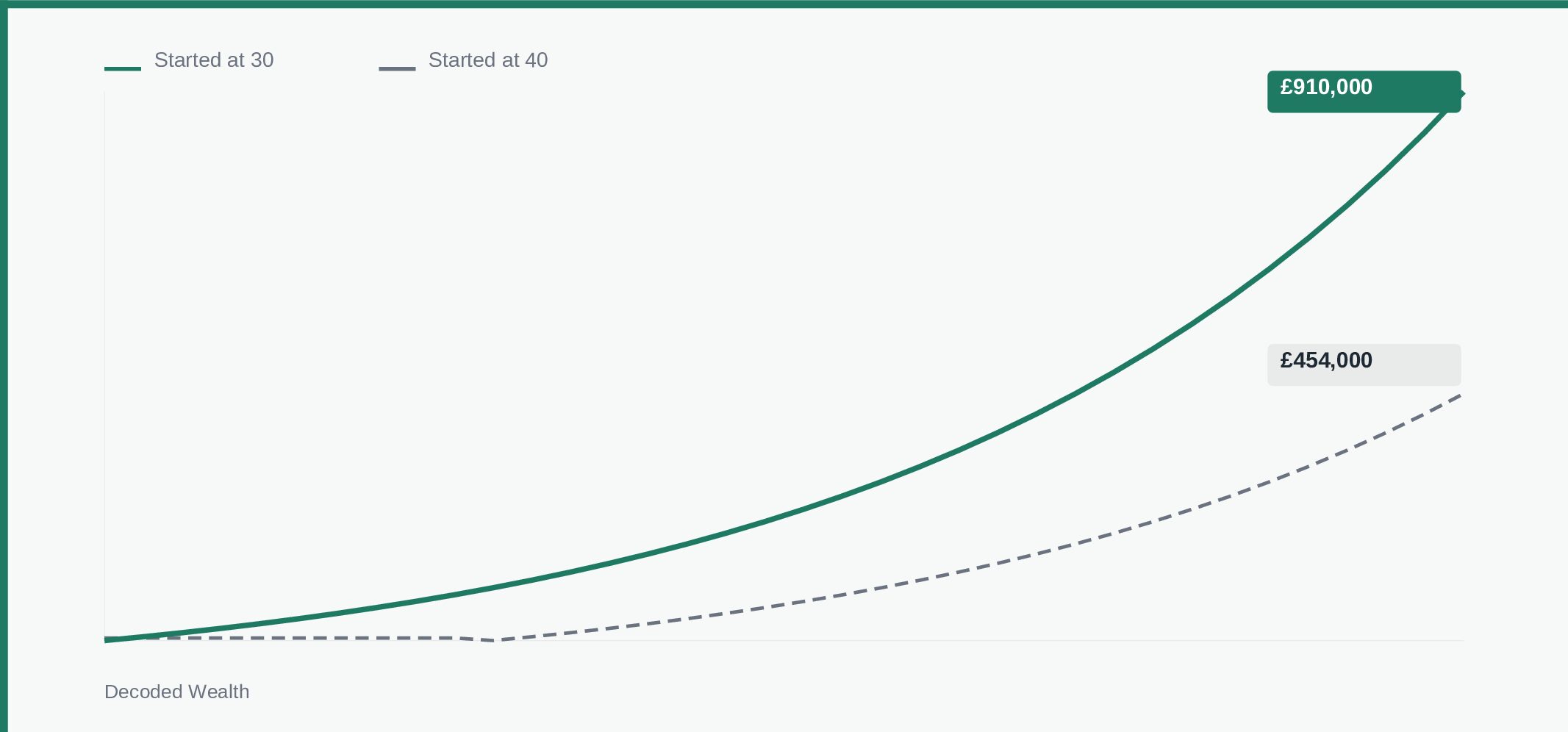

For most people with a long time horizon, a stocks and shares ISA invested in a low-cost global index fund is a very solid choice. You are not trying to pick winners, you are buying the whole market and letting compound growth do its work.

Step 6: Build taxable investments and other assets

This is where wealth actually starts to compound.

Up to this point, you have built stability. From here, you start building scale.

This can include:

– increasing investment contributions beyond your ISA

– building exposure to property (directly or through REITs)

– holding a small allocation to assets like gold as a hedge

– and developing additional income streams

There is no single right answer here. The point is that your money is now working in multiple ways, not just sitting or being saved.

Step 7: Revisit and adjust as your life changes

None of this is set and forget. Life changes. Salaries change. Goals change. Tax rules change.

We review our own finances every few months, nothing obsessive, just a check that the money is going where we want it to go and that our setup still makes sense.

A good habit is a simple annual review at the start of the new tax year in April. Look at your pension contributions, check your ISA, make sure your emergency fund is still the right size for your current life.

A note on order vs. perfection

Get the order right, and everything else becomes easier. This order is a guide, not a rigid rulebook. Some steps overlap. Some people will have good reasons to do things differently. If you have a very generous employer pension match at step four but are still carrying credit card debt, the maths might still favour clearing the debt first. Context matters.

Most people do not fail because they lack discipline.

They fail because they try to build wealth without a structure.

Get the order right, and everything else becomes easier.

The summary version

- Know your numbers. Income minus spending. Fix the gap if there is one.

- Build a one to three-month emergency fund in an easy-access savings account.

- Clear high-interest debt.

- Contribute enough to your pension to get the full employer match.

- Use your ISA allowance. Stocks and shares for the long term. LISA if you qualify.

- Build broader investments and assets when the above is sorted.

- Review regularly. Adjust as life changes.

Capital at risk. Investments can go down as well as up. This article is for informational purposes only and does not constitute financial advice. Decoded Wealth is not regulated by the FCA. Always do your own research before making financial decisions. This article may contain affiliate links. If you use them, we may earn a small commission at no extra cost to you.

2 Comments