Best Stocks and Shares ISA Platforms UK 2026: How to Choose

If you have already decided to open a Stocks and Shares ISA, this article is for you. We are not going to explain what an ISA is or how the tax wrapper works. Our guide to how ISAs actually work covers the full picture. What this is about is the part that comes next: which platform do you actually use?

We spent longer than we should have answering this question ourselves. The honest answer is that the decision matters less than most people think, and more than most comparison sites acknowledge. Here is what we found.

Why the platform question is harder than it looks

There are more than a dozen credible Stocks and Shares ISA platforms in the UK. Most comparison articles rank them by fee, which is useful but incomplete. The platform that costs the least is not always the right answer, because the right platform depends on what you plan to hold, how much you plan to invest, and how much you will actually use it.

A platform with a slightly higher fee that you check monthly and contribute to consistently will do more for your wealth than a zero-fee platform you open and then ignore because the interface frustrates you.

That said, fees compound in the wrong direction over a long time period, and the differences between platforms are real. Understanding what you are paying, and why, is part of being a deliberate investor.

The single most important thing to understand about platform fees

Platforms charge in two main ways: as a percentage of your portfolio, or as a flat monthly or annual fee.

Percentage-based fees are cheaper when your pot is small and more expensive as it grows. A 0.45% annual charge on £5,000 is £22.50 per year. On £100,000, that same rate is £450. If your platform has no cap, the fee grows indefinitely with your portfolio.

Flat fees work in reverse. A £10 monthly fee on a £5,000 portfolio is 2.4% annually, which is very expensive. On a £100,000 portfolio, that same £120 per year is 0.12%, which is very cheap.

The crossover point varies by platform but typically sits somewhere between £20,000 and £50,000. Below that, percentage-based platforms tend to be cheaper. Above it, flat-fee platforms tend to win.

Know which model your platform uses before you open the account.

The platforms we have looked at closely

We are not financial advisers. What follows is our factual understanding of how each platform works. Fees change, so verify directly with the provider before opening an account.

InvestEngine

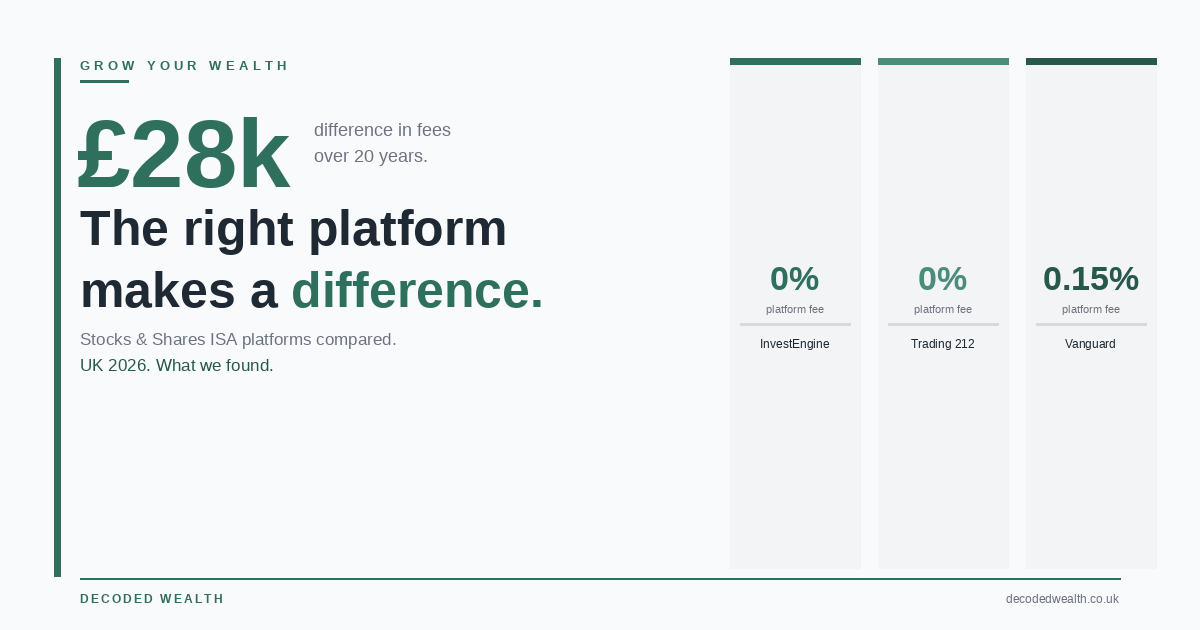

InvestEngine offers a Stocks and Shares ISA with no platform charge for ETF investing. The only cost is the ongoing charge of the ETFs themselves. For someone investing in a single global index ETF, the total annual cost can be well under 0.3%, which is about as low as it gets in the UK market.

The platform is clean, app-first, and straightforward. The fund range is limited to ETFs. For most long-term, index-focused investors, that is not a limitation. For anyone who wants to hold investment trusts or individual shares, it is.

Trading 212

Trading 212 also charges no platform fee on its Stocks and Shares ISA. It holds ETFs and individual shares, so the range is broader than InvestEngine. The interface is polished and accessible. It has become a popular starting point for people investing for the first time.

One thing worth knowing: Trading 212 also offers a contract for difference (CFD) trading product, which is an entirely different, higher-risk product. The ISA and the CFD accounts are completely separate. Make sure you are opening the ISA.

IG

IG is the platform we use for our own Stocks and Shares ISA. We have written about our setup in more detail in our guide to how ISAs actually work, but briefly: we chose IG because of the fund range, the platform stability, and familiarity. It is a broader and slightly more capable platform than the zero-fee options, which suits the way we invest.

IG does charge platform fees, which vary depending on portfolio size and how much you trade. For someone holding a small number of ETFs and contributing monthly, the costs are manageable. For someone with a larger pot investing in funds, it is worth comparing against alternatives.

Vanguard

Vanguard offers a Stocks and Shares ISA with a platform charge of 0.15% per year, capped at £375 annually. The platform is simple and clean. The limitation is that you can only hold Vanguard’s own funds and ETFs.

For someone whose entire investment strategy involves Vanguard funds, that is no constraint at all. For anyone wanting broader access to third-party funds, it is. We use Vanguard for our children’s Junior ISAs. The simplicity of the platform suits that use case well.

Hargreaves Lansdown

Hargreaves Lansdown is the UK’s largest retail investment platform. It offers the widest fund range, strong customer service, and a well-established track record. The fees are higher than most alternatives, starting at 0.45% annually on funds up to £250,000.

For a long-term investor with a growing pot, those fees compound significantly over time. For someone who values breadth of choice and service above cost minimisation, particularly for more complex investment needs, it remains a serious option.

How to decide which one is right for you

There is no single correct answer. There is a sensible framework.

If you are investing in ETFs only and want the lowest possible cost from day one, InvestEngine is hard to argue with on pure fee grounds. If you want a zero-fee platform with slightly broader access including individual shares, Trading 212 is worth looking at. If you want a more established, full-range platform and are comfortable paying for it, IG or Hargreaves Lansdown are considered options, with IG generally more competitive on fees. If your investment strategy is Vanguard funds exclusively, opening directly with Vanguard removes one layer of cost.

For most people starting out, the difference between the zero-fee platforms and the established ones is relatively small in absolute terms when the pot is small. It becomes more meaningful as the portfolio grows, which is exactly when you want to have thought about this already.

The mistake we made

We spent weeks comparing platforms before we opened our ISA. In doing so, we let an entire tax year tick past without contributing anything. The allowance does not carry over. Once 5 April passes, that year is gone.

The platform matters. It matters less than starting. A slightly suboptimal platform that you open and contribute to monthly will dramatically outperform the optimal platform you are still researching.

Pick something credible, open it, and set up a direct debit. You can always transfer to a different platform later if your situation changes or a better option emerges.

What to do

Step 1. Decide what you plan to hold. If it is ETFs only, start with the zero-fee platforms. If you want broader access, move to the full-range options.

Step 2. Estimate your expected portfolio size in one, three, and five years. Use that to think about whether a percentage or flat fee structure benefits you more.

Step 3. Check the specific fund or ETF you want to hold is available on the platform before opening the account. Some platforms limit access to certain providers.

Step 4. Open the ISA before the end of the tax year. The allowance resets on 6 April. Unused allowance from the previous year is gone permanently.

Step 5. Set up a monthly direct debit. The amount matters less than the habit. Even a small monthly contribution, invested consistently, compounds significantly over time.

Step 6. Verify fees directly with your chosen provider before opening. This article reflects our understanding at time of writing, but charges change.

The bottom line

The best Stocks and Shares ISA platform is the one you open, fund consistently, and keep costs low on over time. For most people starting out with ETF investing in the UK, the zero-fee options are genuinely excellent. For those who want more range or are building a larger, more complex portfolio, the established platforms are worth comparing properly.

A slightly imperfect decision made today will outperform the perfect decision you are still searching in six months

Start.

Capital at risk. Investments can go down as well as up. This article is for informational purposes only and does not constitute financial advice. Decoded Wealth is not regulated by the FCA. Always do your own research before making financial decisions. This article may contain affiliate links. If you use them, we may earn a small commission at no extra cost to you.