SIPP Explained: The UK Pension Most Higher-Rate Taxpayers Overlook

Let us explain this the way we wish someone had explained it to us.

When we first started taking our finances seriously, we had three things sitting in roughly the right places. A workplace pension, where money left our payslips each month. An ISA, where we put savings we wanted to grow without paying tax on the gains. And a vague awareness that something called a SIPP existed, which we had filed away as a thing for self-employed people or finance professionals.

That third assumption was wrong. The SIPP turned out to be one of the most powerful tools we had access to all along. We just had not looked at it properly. This is our attempt to explain what it actually is, how it fits alongside your ISA and workplace pension, and why it is particularly valuable if you are a higher rate taxpayer.

What most people assume

Most people assume there are two types of pension: a workplace one provided by your employer, and some kind of private one for when you do not have a workplace option. A SIPP is filed mentally under that second category and never thought about again.

In reality, a SIPP is not a fallback. It is a specific type of pension with distinct advantages, particularly around investment choice and tax relief. It is open to almost anyone in the UK with earnings. And it works alongside a workplace pension rather than instead of it.

The other assumption is that pensions are complicated. They can be. But the core of what a SIPP does is simple once you understand the tax mechanic, which we will get to.

What is actually happening

Think of your financial life as having three main tax-efficient wrappers available to you in the UK. Understanding all three, and what each one does, is genuinely useful.

WRAPPER 1

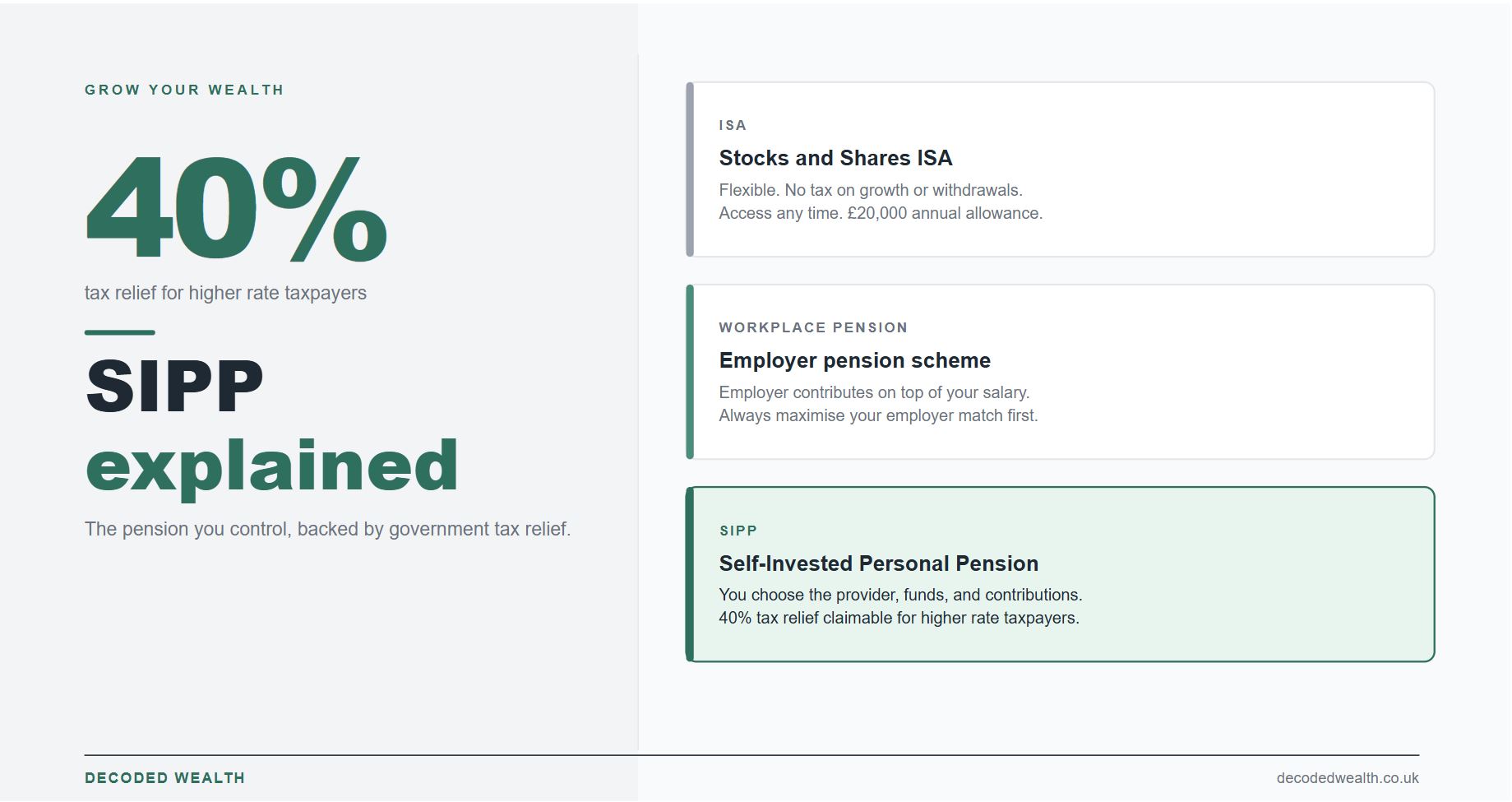

ISA

Contribute money that has already been taxed. Grows tax-free. Withdraw tax-free. Access any time.

Allowance: £20,000/yr

WRAPPER 2

Workplace Pension

Set up by your employer. They contribute on top of your salary. Locked until age 57.

Always maximise employer match first.

WRAPPER 3

SIPP

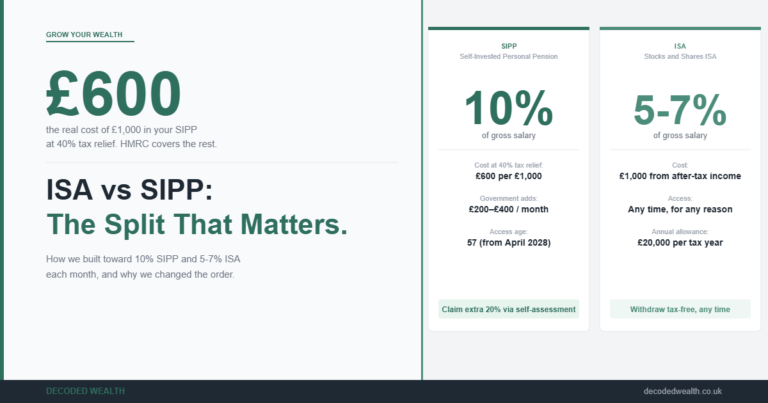

You choose the provider, investments, and contributions. Same tax relief as a workplace pension, full control.

Up to 40% tax relief for higher rate taxpayers.

The fact that in the SIPP the government tops up your contributions based on the tax you pay, is where the SIPP gets interesting.

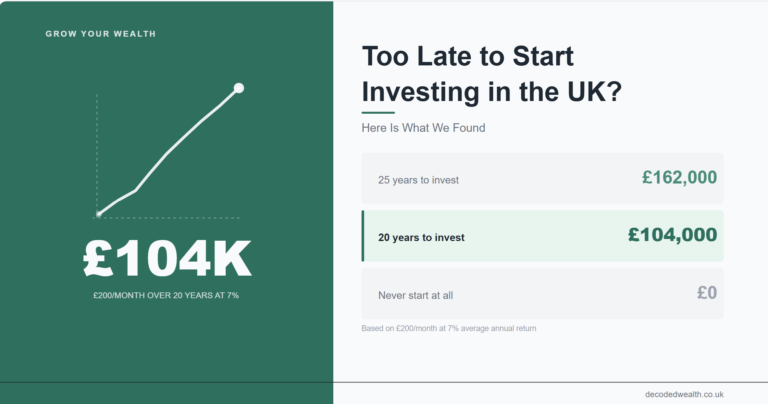

When you contribute to a SIPP, the government adds to your contribution based on the tax you pay. For a basic rate taxpayer, HMRC adds 20%. So you put in £800 and £1,000 lands in the pension. For a higher rate taxpayer, HMRC adds 20% automatically and you can reclaim another 20% through self-assessment. So you put in £600 and £1,000 ends up in the pension, with a £200 tax rebate to follow. That is a 66% return on your contribution before the money has been invested in a single thing.

For someone paying 40% tax, contributing to a SIPP is one of the most efficient financial moves available. The government is handing you back tax you have already paid on that income. Most people in the higher rate tax band either do not know this is possible through a SIPP, or have never been told they need to actively claim the additional relief.

There is also a situation specific to people whose income is between £100,000 and £125,140. In that band, HMRC tapers your personal allowance, creating an effective marginal tax rate of 60% on that income. Pension contributions reduce your adjusted net income. Contribute enough to bring your income below £100,000 and you effectively save 60p for every pound contributed. It is one of the most powerful tax moves in the UK system and it is used by far fewer people than it should be.

What we found

When we finally opened our SIPP properly and started using it, two things became clear.

The first was how much better we felt about our overall pension picture once we could see it clearly. We use Vanguard for our SIPP. We chose it because the platform is genuinely simple, setting up recurring contributions takes minutes, the fund options are clean and sensible, and we could connect our other accounts to get a complete view of where our retirement savings actually stood. Having that visibility changed how we thought about it. It went from background noise to something we actively tracked.

The second was the tax relief. When we first calculated what a higher rate taxpayer was giving up by not maximising pension contributions, the number was uncomfortable. Not because it was catastrophic, but because it had been available all along and we had not been using it. The government contribution is not a bonus or a perk. It is your money being returned to you because you are putting it somewhere that helps you build for retirement. It was always there. We just never went to get it.

A SIPP also became useful for consolidation. Old workplace pensions from previous employers tend to drift. They sit in whatever the default fund was at the time, with charges you have never reviewed, in schemes you barely remember how to log in to. A SIPP is a natural place to bring those together, particularly if the old schemes are standard defined contribution pots without any guaranteed benefits worth preserving.

What to do

Before you open a SIPP, check one thing: whether you are capturing the full employer match from your workplace pension. If your employer contributes 5% when you contribute 5% and you are only contributing 3%, fix that first. Employer match is free money and nothing in a SIPP comes close to it in terms of immediate return.

Once the employer match is secured, think about whether a SIPP makes sense for your situation. It is worth considering if you are a higher rate taxpayer and want to reduce your tax bill while building retirement wealth. It is worth considering if you have old pension pots sitting in schemes you do not actively manage. It is worth considering if you want to invest in specific funds that your workplace scheme does not offer.

Opening one is straightforward. You choose a provider, complete the application online, set up your contributions, and choose your investments. Our choice was Vanguard for the simplicity and low charges. Other well-regarded options include Hargreaves Lansdown, which has the broadest fund range and strong customer service, and AJ Bell, which is competitive on both cost and investment choice.

If you are a higher rate taxpayer contributing through relief at source, which is how most SIPPs work, remember to claim the additional 20% through self-assessment. It does not come automatically. You have to go and get it. But it is yours.

The SIPP sits alongside your ISA and your workplace pension. It does not replace them. Think of the three as each having a specific job: the workplace pension is for employer-matched contributions, the SIPP is for tax-relieved retirement savings where you want full control, and the ISA is for everything you might need before retirement. We walk through the importance of pension and SIPP as a key wealth step in our article.

A SIPP is not complicated once you understand what it is. It is a pension you control, with the same government tax boost as any other pension. For the right person in the right situation, it is one of the best financial tools available in the UK. The question is whether that person is you, and whether you have been leaving the government contribution unclaimed.

Capital at risk. Investments can go down as well as up. This article is for informational purposes only and does not constitute financial advice. Decoded Wealth is not regulated by the FCA. Always do your own research before making financial decisions. This article may contain affiliate links. If you use them, we may earn a small commission at no extra cost to you.