UK Debt Trap 2026: How Easy Credit Quietly Builds Debt

Consumer debt is not just a young person’s problem. Plenty of people are carrying credit card balances, personal loans, and now BNPL (Buy Now Pay Later) commitments that quietly consume a significant portion of their salary before they ever get to think about building anything.

By BNPL we mean services like Klarna, Clearpay, and PayPal Pay in 3 allow purchases to be split into multiple payments, often interest-free at first.

We used credit cards for years before we properly understood the cost. We told ourselves we were managing them fine, because we were not missing minimum payments and not quite at the limit. That felt like control.

It was not control. It was slow-motion drift. The balances crept up. The minimum payments crept up. The amount of our income committed to debt before we made any actual financial decisions crept up. We had the feeling of managing debt without the reality of it.

When we finally sat down and looked at the numbers properly, what we found was uncomfortable. And we think a lot of people on decent salaries are in exactly the same position right now.

What most people get wrong about debt

The most common misunderstanding about consumer debt is that making minimum payments means you are managing it.

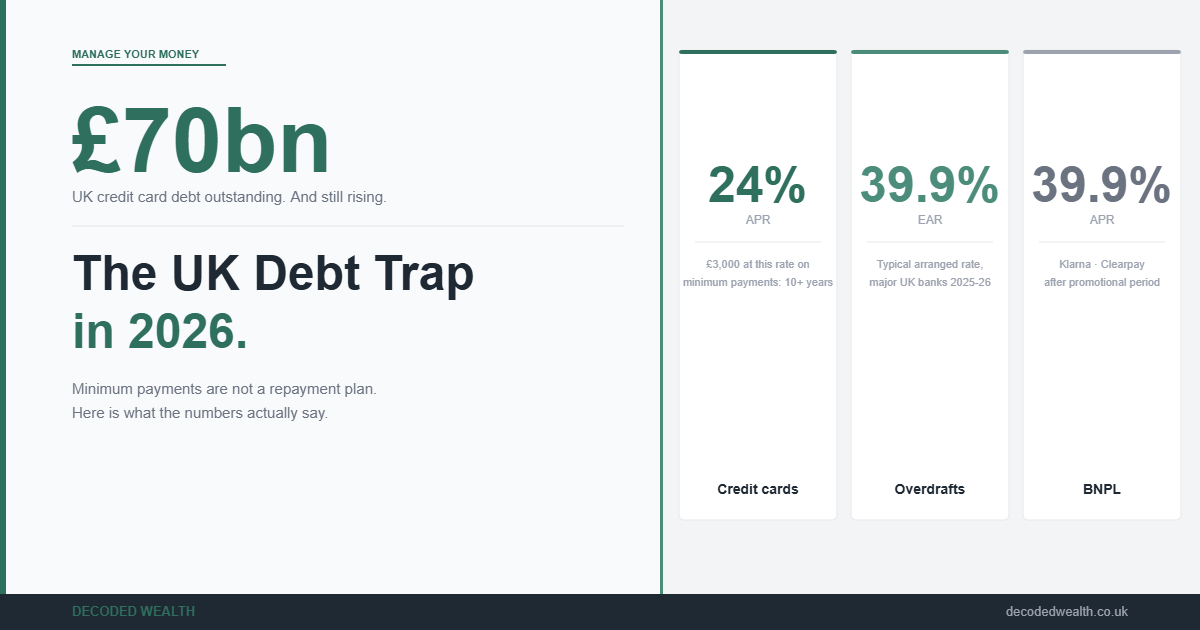

Minimum payments are not a repayment plan. They are the amount designed to keep the debt alive as long as possible while generating maximum interest income for the lender. A credit card balance of £3,000 at 24% APR, paid at minimum payment only, will take well over a decade to clear and will cost nearly as much in interest as the original balance. The maths on this is consistent and rarely shown to borrowers.

Buy Now Pay Later works differently, and the misunderstanding there is different too. BNPL often carries no interest during the promotional period, which makes it feel free. The problem is that it extends spending beyond your actual financial position, and when the promotional period ends or payments are missed, the costs can rise sharply.

The more BNPL commitments you hold simultaneously, the more difficult your cash flow becomes to manage, even before any missed payments arrive. The issue is not just the cost. It is the stacking effect. One BNPL plan rarely causes a problem. Five running at the same time means part of next month’s salary is already spoken for before the month even begins.

The debt problem in the UK is not that people are irresponsible. It is that the friction of spending has been deliberately reduced to the point where it does not feel like a decision. A tap on a phone or a BNPL split at checkout does not activate the same psychological response as handing over cash or even typing in a card number.

What is actually happening in the UK right now

Consumer debt in the UK is growing across all age groups, not just younger cohorts.

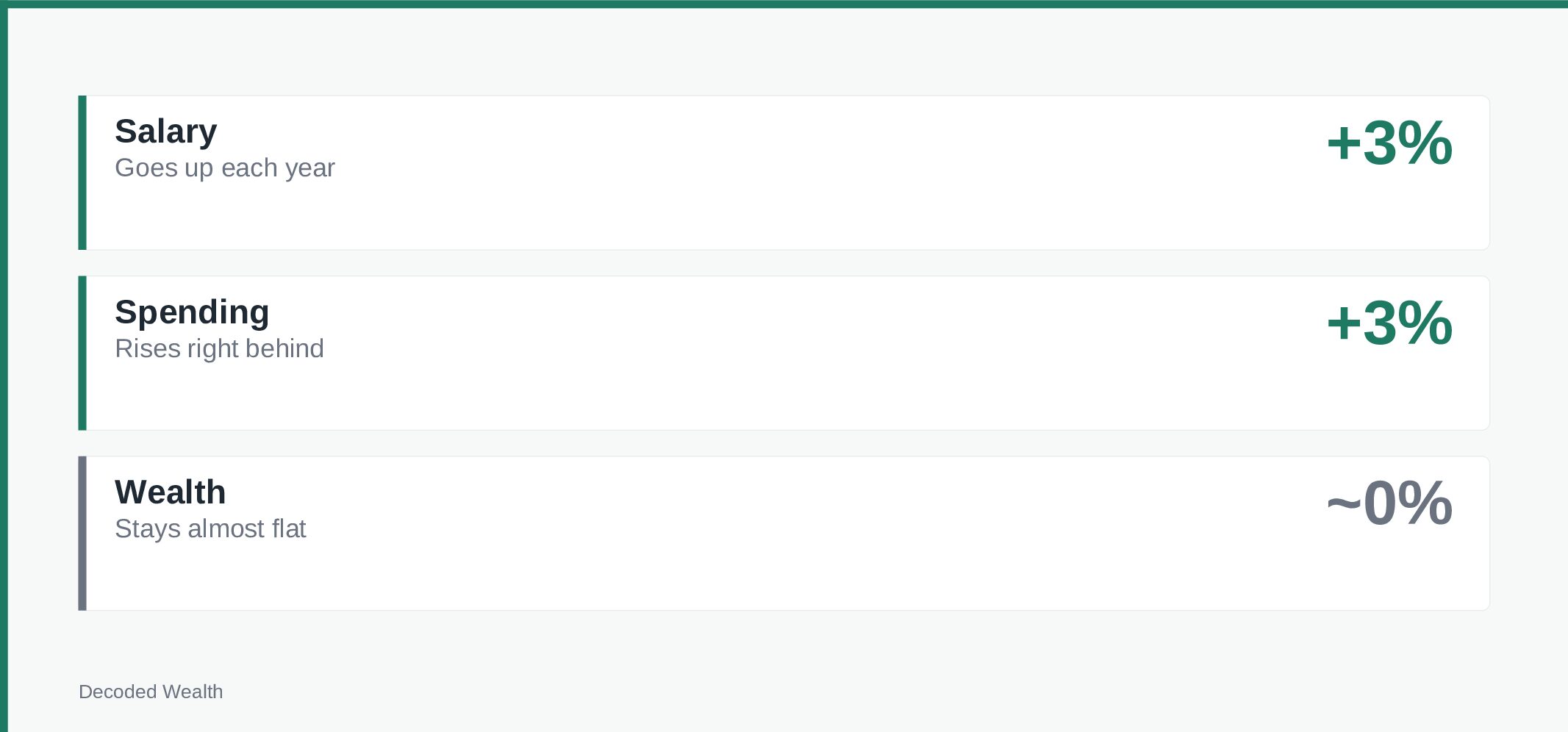

What is unusual about the current debt cycle is that it is happening during relatively strong employment and rising salaries. Debt is no longer just a symptom of financial distress; it is becoming part of everyday spending behaviour

The Bank of England reports that UK credit card balances have risen consistently through 2025 and into 2026 and UK credit card borrowing alone now sits well above £70 billion.

BNPL providers processed billions of pounds in transactions in the UK last year. Debt charities including StepChange and the Money Charity consistently report that average unsecured debt among clients is rising, with many carrying debt from multiple sources simultaneously: credit cards, BNPL, overdrafts, and in some cases personal loans stacked on top of each other.

What has changed in recent years is the normalisation. High-cost short-term debt used to carry social weight. BNPL and contactless spending have largely removed that. Spending above your means has been repackaged as financial flexibility, and a generation of people has grown up in a financial environment where carrying balances feels ordinary.

There is also a part of the debt system that many people simply do not understand: what happens to very old debts. Old debts do not disappear after six years, but under the Limitation Act 1980, they become statute-barred, meaning lenders can no longer successfully take you to court to recover them in England and Wales. Debt collection companies sometimes pursue statute-barred debts aggressively anyway, and many people pay them without realising they had a legal right not to. Knowing your rights on old debt is part of understanding what you actually owe and what you are genuinely obligated to pay.

What we found

When we properly audited every financial commitment we had, we found the numbers were clearer than we expected, and the path out was more straightforward than the anxiety around the debt had made it feel.

The thing that made the biggest practical difference was seeing all the debt in one place. Not knowing the exact total is part of what sustains the anxiety. Writing it all down, every balance, every interest rate, every minimum payment, made it a problem with a defined edge rather than an indefinite cloud.

The approach we used after that was what is usually called the avalanche method: directing any money available beyond minimum payments toward the highest-interest debt first, regardless of the balance size. The maths of this approach saves the most money overall. For debts at 20% to 25% APR, the difference over a year of focused repayment is significant.

The psychological shift was as important as the method. Treating the debt as a problem to be solved, with a specific plan and a specific timeline, changed how we thought about every other spending decision in the meantime. Our multi-account system helps you separate debt repayment money from everyday spending.

What to do

Step 1. Do a full debt audit.

Write down every debt you currently hold. Credit cards, BNPL commitments, overdraft, personal loans. For each one: the current balance, the interest rate, and the minimum monthly payment. If you have lost track of a debt, check your credit report on Experian, Equifax, or TransUnion. All three offer free access to your report.

Step 2. Order them by interest rate, highest first.

This is the starting point for the avalanche method. The highest-rate debt is costing you the most money per month and should be cleared first, regardless of whether the balance is the largest.

Step 3. Pay the minimum on everything except the highest-rate debt.

Direct any additional money you can find toward the highest-rate debt. When that is cleared, move the full amount you were paying on it to the next highest-rate debt. This is the compounding effect working in reverse.

Step 4. Stop adding to the debt while you are clearing it.

This sounds obvious. In practice it is the step that determines whether the plan works. Debt reduction only happens when repayments are larger than new spending. New spending that matches your repayments keeps you static, not progressing. We cover how spending quietly keeps pace with income in this article

Step 5. List all BNPL commitments separately.

BNPL does not always appear on your credit file, which means it is easy to underestimate your total monthly commitments. Write down every active BNPL plan: the provider, the remaining balance, and the remaining payment schedule. Include this in your monthly outgoings calculation.

Step 6. Know your rights on old debts.

If a debt is more than six years old and you have not made a payment on it or acknowledged it in writing since, it is likely statute-barred in England and Wales. The creditor can still contact you, but they cannot successfully sue to recover it. If a debt collector contacts you about a debt you believe may be old, contact Citizens Advice before making any payment or acknowledging the debt in any form. Making a payment on a statute-barred debt can restart the limitation period.

Most people do not escape the debt trap by earning more. They escape it by making the system visible and applying a plan consistently.

Capital at risk. Investments can go down as well as up. This article is for informational purposes only and does not constitute financial advice. Decoded Wealth is not regulated by the FCA. Always do your own research before making financial decisions. This article may contain affiliate links. If you use them, we may earn a small commission at no extra cost to you.