ISA vs SIPP in the UK: The Exact Split We Use and the 40% Tax Relief Surprise

We had a stocks and shares ISA running for years before we ever opened a SIPP. The ISA made sense from the start: put money in, it grows, you can get to it whenever you need. Familiar, flexible, and easy to understand. We had a workplace pension ticking along in the background and assumed between those two we had the savings picture covered.

We did not. When we finally sat down and worked out what higher rate tax relief on SIPP contributions actually meant in practice, not in theory, but in actual pounds returned to our bank account, the whole picture shifted. Not just the maths. The way we thought about every pound we earned.

This is the version of the ISA vs SIPP conversation we wish someone had given us three years earlier.

What most people do wrong

The pattern most people in the higher rate tax band follow is the one we followed for too long. Workplace pension at the employer match, ISA when there is money left over, and the assumption that is a sensible approach.

It is not wrong. It is just incomplete.

The mistake is treating the ISA as the default destination for additional savings and never seriously considering what a SIPP adds on top. A SIPP is not a backup option for people without a workplace pension. It is a separate, active tool that sits alongside both your workplace pension and your ISA. And for anyone paying 40% income tax, it carries a feature no ISA can match.

The other mistake is treating the two as competitors. They are not. They have different jobs. The question is not ISA or SIPP. The question is how much goes into each one and why.

What is actually happening

Here is the mechanic, as plainly as possible.

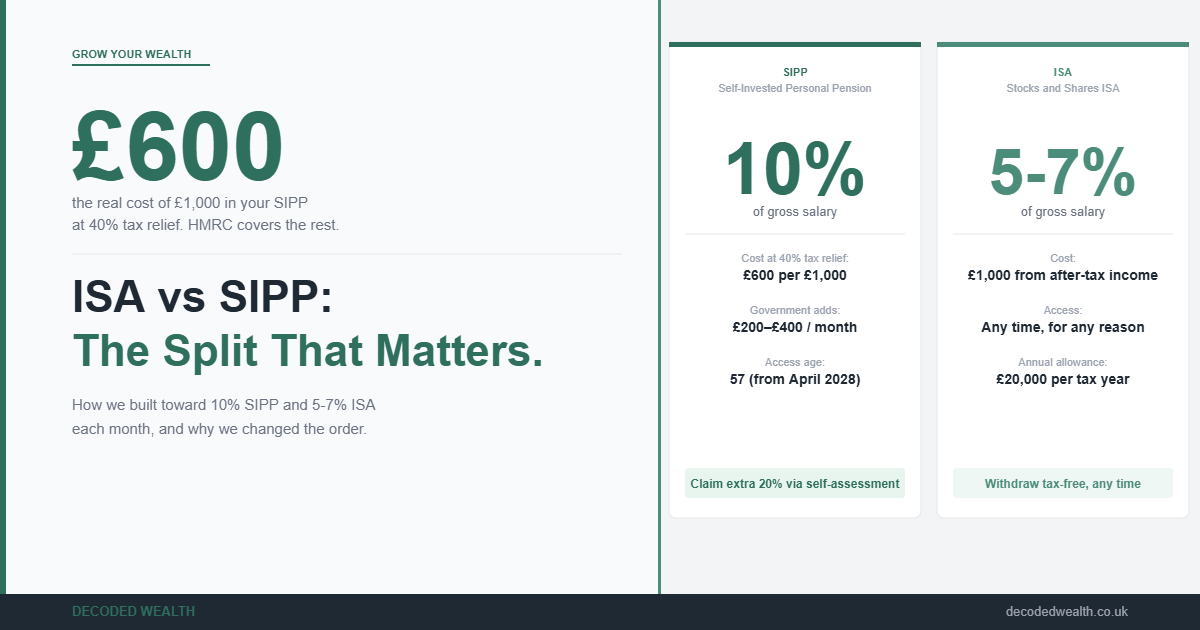

When you contribute to a SIPP, HMRC adds tax relief at your marginal rate. For a basic rate taxpayer, every £800 you put in becomes £1,000 in the pot. For a higher rate taxpayer, every £600 you contribute becomes £1,000 in the pot, with another £200 coming back via self-assessment. You are not receiving a bonus. You are getting back tax you already paid on that income.

That difference in real cost changes the comparison completely. If you earn £60,000 and want £1,000 working for your retirement, you can either put £1,000 of after-tax income into an ISA or you can put £600 into a SIPP and let HMRC cover the other £400. Both result in £1,000 invested. Only one costs you £600.

The allocation we work toward, based on a salary around £60,000:

SIPP: 10% of gross salary. That is £6,000 per year, or £500 per month gross. At 40% tax relief, the real net cost is approximately £300 per month. The government adds the remaining £200.

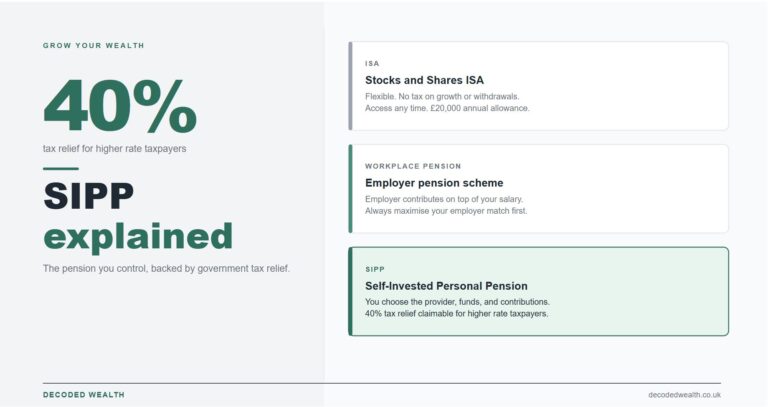

ISA: 5% to 7% of gross salary. That is £3,000 to £4,200 per year, or £250 to £350 per month from post-tax income.

This is in addition to whatever goes into the workplace pension to capture the full employer match. The employer match always comes first. Everything else is built from there.

These percentages are targets, not starting points. We did not get to 10% SIPP from day one. We got there in stages over roughly two years, and it took seeing the actual self-assessment rebate before we committed to accelerating.

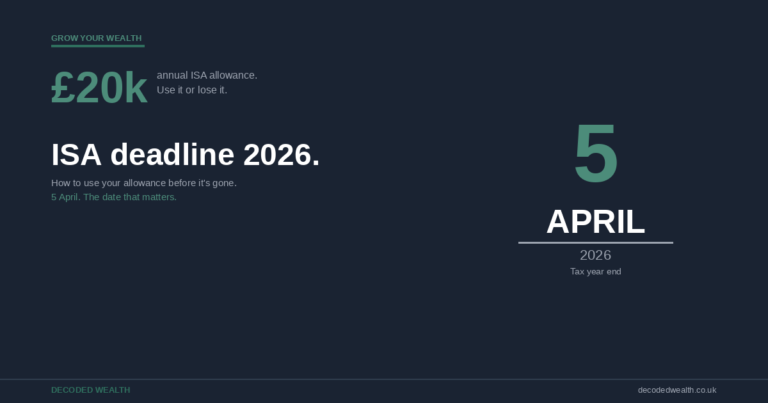

A few rules worth knowing. The annual pension allowance is £60,000 per year, or 100% of your earnings if lower. If you contribute to both a workplace pension and a SIPP, both count toward that allowance. The ISA allowance is £20,000 per tax year. Neither wrapper charges tax on investment growth. The SIPP taxes withdrawals in retirement as income. The ISA does not.

What we found

When we opened our SIPP, we put in a small amount. Maybe 3% of salary. Not because we could not afford more, but because we were not fully convinced it was worth prioritising over ISA contributions. The ISA felt real and accessible. The SIPP felt locked away and abstract.

The thing that changed it was the self-assessment return.

At the end of that first tax year, we claimed the higher rate relief on our SIPP contributions. On around £3,600 contributed, we got £720 back. Not a projection. An actual bank transfer from HMRC. It landed in our account and felt entirely different from anything we had read about it in the abstract. It was money we had already paid in tax, being returned to us because we had directed those earnings into a pension wrapper.

We increased the SIPP contribution the following month.

From 3%, we moved to 6%. Then to 10% once we looked at the whole picture: how contributions interacted with our overall tax position, what it would compound to over a fifteen to twenty year horizon, and how little it actually cost us in take-home pay relative to what was landing in the pension. At 40% relief, a £500 gross SIPP contribution costs us £300 per month in actual spending power. The other £200 is ours, sitting in a pension wrapper, growing tax-free.

The ISA did not stop. It runs alongside, doing a different job. We use it for money we might want access to before pension age: medium-term investment goals, a tax-free pot we could reach if circumstances change. We do not treat the ISA as secondary. We treat it as the right tool for a different pool of money.

The thing we genuinely wish someone had told us earlier is this: the SIPP and ISA are not in competition. They solve different problems. The SIPP solves the problem of tax-efficient retirement savings where you can tolerate the lock-in. The ISA solves the problem of accessible, flexible investment growth. Run both, in the right proportions, and you are using two of the most powerful financial tools available to UK earners at the same time.

What to do

Step 1. Take the full employer match on your workplace pension, no exceptions.

If your employer will contribute an additional percentage of your salary conditional on you contributing, that contribution is a pay rise in everything but name. Maximise it. If you do not know your employer’s match terms, check today.

Step 2. Open a SIPP if you do not have one.

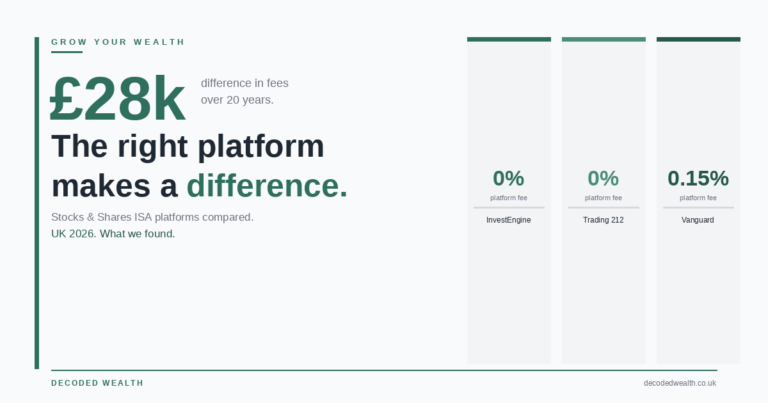

Opening a SIPP takes roughly twenty minutes online. We use Vanguard for ours. It is clean, low cost, and straightforward to set up recurring contributions. AJ Bell is also worth looking at for a broader investment range. Hargreaves Lansdown if you want the widest fund options and strong customer service. Our full SIPP guide walks through what to look for in choosing a provider.

Step 3. Start your SIPP contribution at whatever is realistic, and build toward 10% of gross salary.

10% of gross salary into the SIPP is a meaningful target for higher rate taxpayers. On a £55,000 salary that is £458 gross per month, which costs around £275 net after 40% relief. You do not need to start there. We did not. Start at 3% or 5%, contribute for a year, claim your first self-assessment rebate, and then decide whether to increase. The rebate tends to do the persuading.

Step 4. Allocate 5% to 7% of gross salary into a stocks and shares ISA.

This is for money with a time horizon shorter than retirement, or for any savings you want to be able to access before age 57. If your emergency fund is already in place, this is your accessible investment pot outside the pension wrapper. We cover how the ISA wrapper works in our stocks and shares ISA explainer, and which platforms we actually use and rate in our ISA platforms guide.

Step 5. Claim your higher rate relief every year via self-assessment.

SIPP providers using relief at source, which most retail platforms do, automatically claim 20% from HMRC on your behalf. The additional 20% for higher rate taxpayers does not come automatically. You have to submit a self-assessment return and claim it. It is your tax money. Go and get it every year.

Step 6. If your income falls between £100,000 and £125,140, treat SIPP contributions as a priority.

In that band, HMRC tapers your personal allowance and creates an effective marginal tax rate of 60% on that income. Every pound contributed to your SIPP reduces your adjusted net income. Bring your income below £100,000 through SIPP contributions and you restore your full personal allowance and remove that 60% rate. The salary sacrifice article covers how pension contributions through your employer can achieve the same effect without needing a separate SIPP claim.

The ISA and the SIPP are two wrappers doing two different jobs. The ISA gives you flexibility and tax-free access whenever you need it. The SIPP gives you the government’s contribution on top of your own money, locked away until you stop working. Both are genuinely useful. The mistake is running only one of them, or running them without understanding what each one is actually doing. Once you see the numbers clearly, the split almost decides itself.

Capital at risk. Investments can go down as well as up. This article is for informational purposes only and does not constitute financial advice. Decoded Wealth is not regulated by the FCA. Always do your own research before making financial decisions. This article may contain affiliate links. If you use them, we may earn a small commission at no extra cost to you.