Student Loan UK: How It Quietly Holds Back Your Wealth

We did not graduate with student debt. We mention this upfront because it is relevant to how this article came to exist.

For a long time, it meant we had a blind spot. We knew Plan 2 loans were different from traditional debt, but we had never really questioned how they worked in practice.

We had absorbed the standard framing: the repayments are small, they come out automatically, they get written off eventually. Nothing to worry about.

Then someone close to us, earning well into their forties, sat down and walked us through their monthly pay in detail. They were not struggling in any obvious way. They had a good salary and a stable job. But they could not work out why, despite earning what felt like enough, they had almost nothing left to build with each month.

When we looked at the breakdown properly, the student loan repayment was sitting in the middle of it. Taking 9% of everything above a certain threshold. They had been paying it for over fifteen years. They had never really thought about what it was doing.

We started looking at the numbers more carefully. What we found surprised us.

It also explained something we had seen repeatedly but never fully understood: people earning good money, but still feeling stuck financially.

What most people assume

The standard framing of Plan 2 student loans is that they are nothing to worry about. You only repay above a threshold, you repay a small percentage, and it gets written off after 30 years. The government does not chase you aggressively. It comes out automatically. Forget about it.

Most graduates in their 30s and 40s have absorbed exactly that message, usually from the same institutions that sold them the loan.

The problem is that “nothing to worry about” and “invisible impact” are not the same thing.

Most graduates at the peak of their earning years are walking around with something that adds 9% to their effective tax rate on every pound they earn above £27,295. They may have never thought about it in those terms. They are likely to be at the point in their career where the deduction hits hardest, earning well enough to feel it sharply but not so well that it feels trivial. And many have no idea it has already changed what a bank will lend them.

What is actually happening

Plan 2 student loan repayments are 9% of everything you earn above the threshold, which sits at £27,295 a year in 2025/26.

At that rate, here is what the numbers look like in practice.

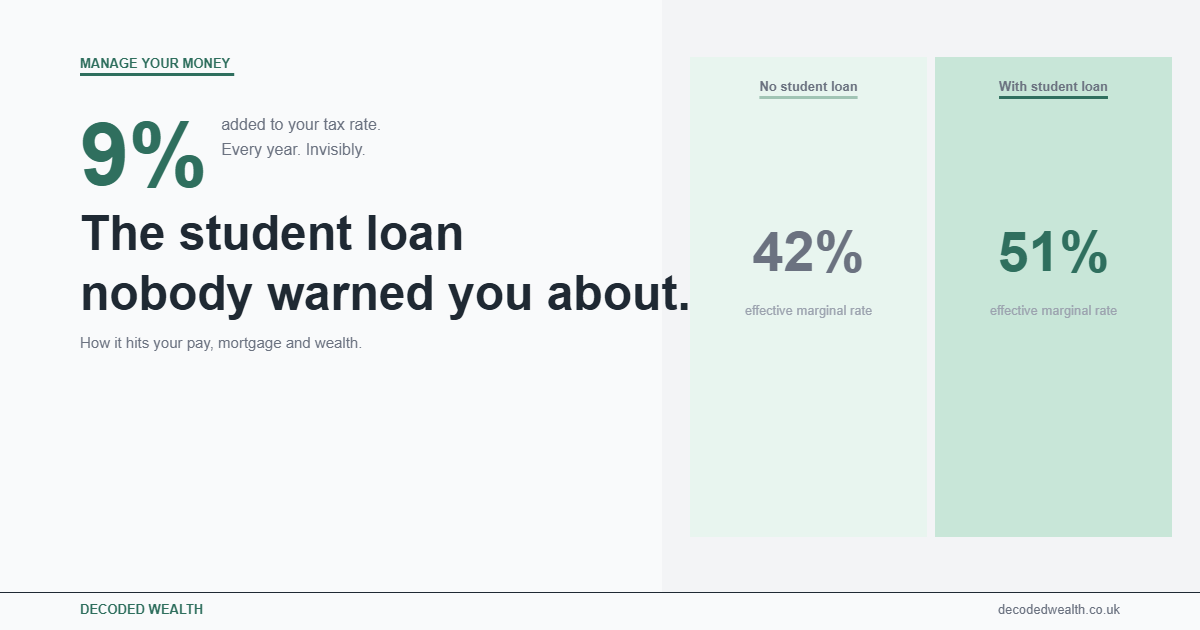

If you earn £45,000, you pay 20% income tax on earnings above the personal allowance, 8% National Insurance on earnings in the basic rate band, and 9% student loan repayments on earnings above the threshold. In a single payslip, that is an effective deduction rate of 37% on a significant chunk of your salary before it reaches you.

For anyone earning between £50,270 and £100,000, the rate climbs further. National Insurance drops but income tax rises to 40%, so the combined marginal rate on each extra pound including the student loan is closer to 51%. More than half of every additional pound earned is leaving before you decide what to do with it.

This is not a catastrophe. But it is real money, and it affects everything from how quickly you can build savings to what a mortgage lender will offer you. If you are unsure what “enough” looks like, we break down how much you should realistically be saving each month.

The mortgage impact is the part nobody mentions at the point when it would actually be useful to know. Lenders calculate affordability based on net income, and student loan repayments reduce net income. When you apply for a mortgage, the lender factors in your repayment as a monthly commitment. That reduces your borrowing ceiling at exactly the moment you are trying to buy a home.

For a borrower earning £40,000, a £200 monthly student loan repayment could reduce the maximum mortgage offered by around £40,000 to £50,000, depending on the lender’s approach. On a market where the average UK house price is still above £280,000, that gap matters.

What we found when we looked properly

When we modelled what the person we mentioned at the start had actually paid over fifteen years, and what they were likely to pay over the remaining fifteen, the numbers were more significant than either of us had assumed.

The first thing we found is that for many graduates, the loan does not behave like a traditional debt. If you do not earn consistently above the threshold, repayments are low and the balance can grow with interest in the meantime. A significant proportion of borrowers will never repay their full balance and will have the remainder written off.

The second finding was less comfortable. For those who earn well and consistently, the loan behaves more like a tax than a debt. You will repay far more than you originally borrowed, possibly double, spread invisibly across decades. On a £40,000 original loan, a graduate who earns well could repay £80,000 or more before the write-off point. That is not an argument against having gone to university. It is an argument for understanding what you are actually paying.

The third thing we found, and the one that changed how we now talk about this with people, is that the most common advice on this topic is often wrong. Specifically, the idea that making voluntary overpayments is a sensible thing to do.

For most graduates, overpaying is not sensible. The interest rate on Plan 2 loans is capped at RPI plus 3%, and the write-off after 30 years means that additional voluntary repayments may never reduce what you repay in total. If your income trajectory means you are going to repay the full balance regardless, additional payments have no long-term benefit. The money is almost always better directed elsewhere first.

What to do

Step 1. Find out which Plan you are on.

If you started university in England or Wales between 2012 and 2023, you are on Plan 2. If you started in 2023 or after, you may be on Plan 5 with a different threshold and write-off period. If you studied before 2012, Plan 1 applies with different rules. The Student Loans Company holds your records and can confirm your plan, your current balance, and your repayment history.

Step 2. Calculate your actual monthly repayment.

Take your gross annual salary. Subtract £27,295 (the Plan 2 threshold for 2025/26). Multiply the remainder by 9%. Divide by 12. That is your monthly repayment. If you earn £38,000, that is approximately £81 per month. Write it down and include it in your committed monthly outgoings, not as a footnote.

Step 3. Build your financial plan from your actual net figure.

The student loan repayment leaves before your salary arrives. It is not discretionary spending. When you calculate how much you have available each month, start from the number that actually hits your account, not the gross figure on your contract. Most people who feel confused about where their money goes are working from the wrong starting number.

Step 4. Before applying for a mortgage, understand the affordability impact.

Speak to a mortgage broker and be specific about your student loan balance and monthly repayment. A good broker will tell you how it affects your borrowing with different lenders. Some lenders are more generous in their treatment of student loan repayments than others, and knowing this before you start the process saves significant frustration.

Step 5. Think carefully before making voluntary overpayments.

Unless you have a high income trajectory and a realistic expectation of repaying the full balance within the 30-year window, voluntary overpayments are unlikely to reduce your total repayment. For most people, the money is better used building an emergency fund, taking the employer pension match, or filling an ISA first. The calculation depends heavily on your income trajectory, and how that evolves over time is often more important than the starting salary itself, we break it down here.

Step 6. Do not let the student loan crowd out more urgent financial priorities.

The student loan is a managed deduction. An employer pension match is free money you lose permanently if you do not take it. These priorities are not a close call. Build the emergency fund, take the pension match, then use your ISA allowance, making sure you understand how ISAs actually work in practice before committing long term. Then, if there is anything left and the numbers genuinely support it, consider the overpayment question.

We came to this topic from the outside, and that turned out to be useful. When you have not been told since the age of eighteen that your student loan is not really debt and that you should not worry about it, the numbers look different. They look like what they are: a 9% additional deduction on a significant portion of your income, with a real impact on your mortgage affordability and your long-term wealth-building capacity. Understanding it clearly is not about worrying. It is about making better decisions with the money that actually reaches you.

Capital at risk. Investments can go down as well as up. This article is for informational purposes only and does not constitute financial advice. Decoded Wealth is not regulated by the FCA. Always do your own research before making financial decisions. This article may contain affiliate links. If you use them, we may earn a small commission at no extra cost to you.