Waiting to invest has a real cost. See how delaying impacts your wealth in the UK and why starting early matters more than getting it right.

For years we did not invest. We had the intention, we had the rough idea, and we had every reason in the world not to start.

Which platform do you pick? There are dozens. Which funds? Thousands. How much should you put in? What if you pick the wrong thing? What if the market crashes the week after you start? What if you should have waited for a better moment?

So we researched. And researched. And read more. And compared more platforms. And convinced ourselves we were not quite ready yet. This went on for longer than we are comfortable admitting.

The thing nobody told us clearly enough is this: the research phase has a cost. Every month you spend getting ready to invest is a month your money is not growing. And that cost compounds, quietly, invisibly, until one day you do the maths and realise what the delay actually meant in real money.

That calculation was uncomfortable. This article is the one we wish someone had put in front of us earlier.

Most people think the risk is investing. The real risk is waiting.

What the delay actually costs you

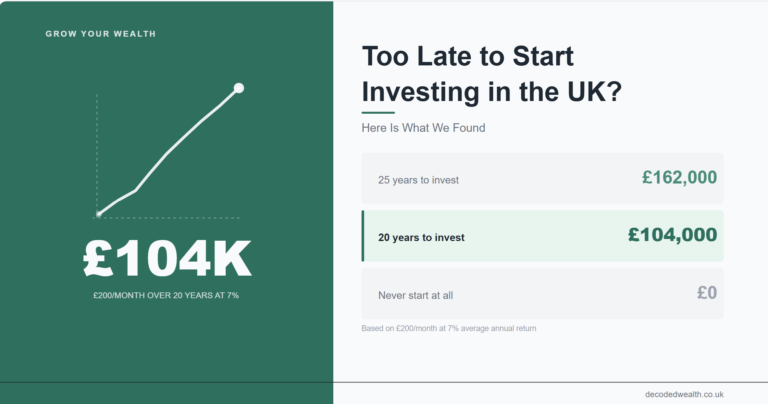

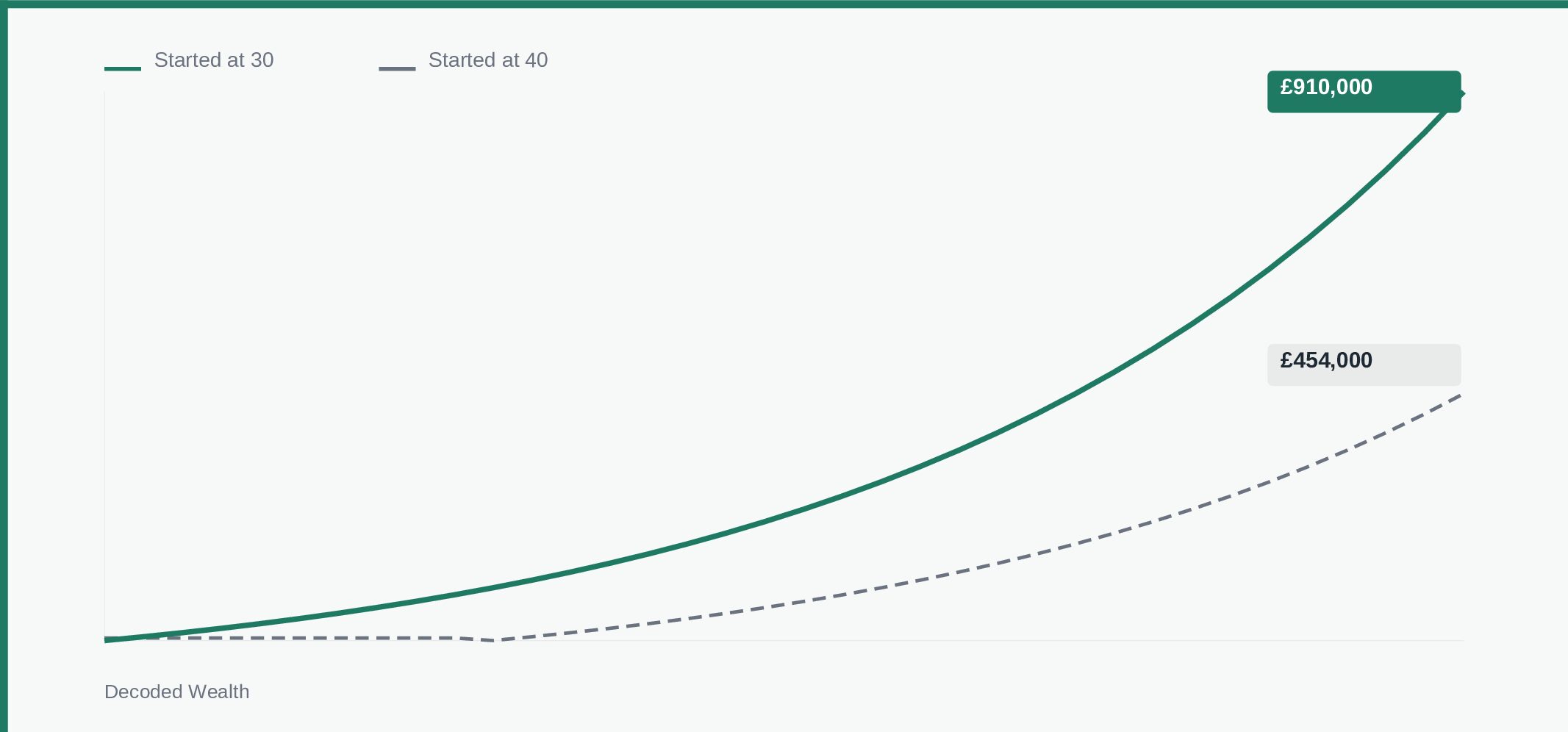

Here is a straightforward example. Two people each invest 300 pounds a month into a stocks and shares ISA. One starts at 30. One starts at 40. Both get an average annual return of 7 percent, which is roughly in line with long-term historical returns for a globally diversified portfolio. Both stop contributing at 65.

The person who started at 30 ends up with roughly 910,000 pounds.

Who started at 40 ends up with roughly 454,000 pounds.

Same monthly amount. Same return. One decade of difference. The gap between them is around 456,000 pounds.

That is not the cost of picking the wrong fund. That is not the cost of bad timing. That is purely the cost of starting ten years later. The extra decade of contributions matters, but so does the decade of compound growth on everything that was already in the pot.

This is why starting, even imperfectly, is almost always better than waiting until everything feels right. If you want a clear structure of what to prioritise first, our seven-step wealth-building guide lays it out simply.

Why not starting feels safer than it is

Cash in a savings account has a stable number on the screen. It does not go up and down. It does not give you a bad week. When markets fall and the news is grim, the cash sitter feels vindicated.

But cash has a risk too. It just does not show up on an app. It shows up in purchasing power. As of early 2026, the best easy-access savings accounts are paying around 4.5 to 4.75 percent. With UK inflation still running above 3 percent, the real return on cash, what your money actually buys in the future, is thin. Over a decade, a savings account that just about keeps pace with inflation has not built wealth. It has preserved it, barely, while a diversified investment portfolio has likely grown in real terms by a significant margin.

The risk of investing is visible. A bad month shows up in red on your screen. The risk of not investing is invisible. It shows up twenty years later as a retirement pot that is half the size it could have been, and by then there is nothing you can do about it.

What getting it wrong actually looks like

The fear of making a bad investment is real and we understand it completely because we felt it too. But here is the honest picture of what getting it wrong looks like for a long-term investor with a sensible approach.

If you invest in a broad global index fund inside a stocks and shares ISA and the market drops 30 percent in a bad year, your 10,000 pounds becomes 7,000 pounds on paper. That feels genuinely awful. We are not going to pretend otherwise.

But if you leave it alone and keep contributing, history is unambiguous: markets have recovered from every significant fall they have ever had. Every single one. The 2008 financial crisis. The 2020 pandemic crash. Every other major downturn in modern investing history has been followed by recovery and then new highs.

The investors who lose money permanently are almost always the ones who sell during the panic. The ones who do well over time are usually the ones who held on, or better still kept buying while things were cheap.

Getting it slightly wrong by choosing a fund with marginally higher fees, or a slightly different mix of assets, is a much smaller problem than not starting. A mediocre investment made early almost always outperforms a perfect investment made ten years later.

The paralysis trap and how to get out of it

We spent years in research mode. Reading books, comparing platforms, building spreadsheets comparing fund performance, trying to predict which markets would do better. All of it felt productive. Almost none of it was necessary before making a start.

Here is the structure that would have got us moving years earlier, and the one we would give to anyone starting from zero today.

- Open a stocks and shares ISA with a straightforward platform. For beginners we have used and rate IG for flexibility and breadth. Trading 212 is genuinely fee-free and easy to navigate. Vanguard is simple and cheap. Pick one. Do not spend three months comparing them all. If you are not fully clear on how ISAs actually work, we break it down simply in our ISA guide.

- Choose one broad global index fund or ETF. Something that tracks the whole world market, not one country, not one sector. This single decision gives you exposure to thousands of companies in one go. It is not exciting. It is effective.

- Set up a monthly contribution by direct debit. Even 50 pounds a month. Make it automatic so it happens whether or not you remember. Having your money structured properly makes this much easier to stick to over time.

- Leave it alone. Check it every few months if you want. Do not check it every day. Short-term movements are noise. Long-term direction is what matters.

That is genuinely 80 percent of what you need to do. The remaining 20 percent, learning more, optimising, diversifying further, can come later once you are in the habit and the money is already working.

The biggest investment decision you will ever make is the one you actually make. Not the perfect one you are still planning.

Where to go from here

If you have not opened a stocks and shares ISA yet, that is the first step. Our ISA guide covers the different types, what we use ourselves, and exactly how to open one in about fifteen minutes. Our investing guide goes deeper on what to put inside it and why we focus on broad, low-cost funds rather than individual stocks.

Start there. Then come back and keep reading. The most important thing is that you start.

Capital at risk. Investments can go down as well as up. This article is for informational purposes only and does not constitute financial advice. Decoded Wealth is not regulated by the FCA. Always do your own research before making financial decisions. This article may contain affiliate links. If you use them, we may earn a small commission at no extra cost to you.