Redundancy in the UK: What You’re Owed, What to Do, and How to Come Out Ahead

We have not been made redundant. We want to say that upfront. The people who have been through it have an experience we cannot claim.

What we can say is that we have watched people close to us go through it. More than once. The financial reality was almost always different to what they expected. Not always worse. Often just different. And the gap between expectation and reality came down to one thing: not knowing the numbers before the moment arrived.

The employment market has shifted. AI-driven restructuring. Consolidation across sectors that felt stable. Cost pressures reaching organisations that seemed protected. Redundancy is now touching people who never saw it coming. They are getting as much warning as everyone else. Which is not much.

What most people do wrong

Most people do not know their full entitlements before the HR conversation. They negotiate from uncertainty. They may accept a package without knowing whether it meets the statutory minimum, whether it exceeds it, and whether any excess is structured in a tax-efficient way.

The second mistake is spending the lump sum too quickly. For someone with a new role lined up within weeks, the payment works as a bridge. For someone facing a restructured market who needs to wait, retrain, or relocate, spending it immediately removes the only buffer they have.

The third is missing the pension question entirely. Employer contributions during notice periods and garden leave are a detail most people never raise.

What is actually happening

Eligibility first.

Statutory redundancy pay requires at least two years of continuous service with the same employer. Under two years means no statutory entitlement. That does not mean no payment. Some employers pay contractual or ex-gratia amounts regardless of service length, particularly during large-scale restructuring. Always ask, even without the statutory minimum behind you.

How statutory pay is calculated.

The calculation uses three variables: age band, length of service, and weekly pay. Service is capped at 20 years. Weekly pay is capped at £751 from 6 April 2026.

| Age during service | Weeks’ pay per full year |

|---|---|

| Under 22 | 0.5 weeks |

| 22 to 40 | 1 week |

| 41 or over | 1.5 weeks |

The maximum statutory payment from 6 April 2026 is £22,530. Most employers with redundancy policies pay above this. The contractual redundancy figure is what matters.

Tax treatment.

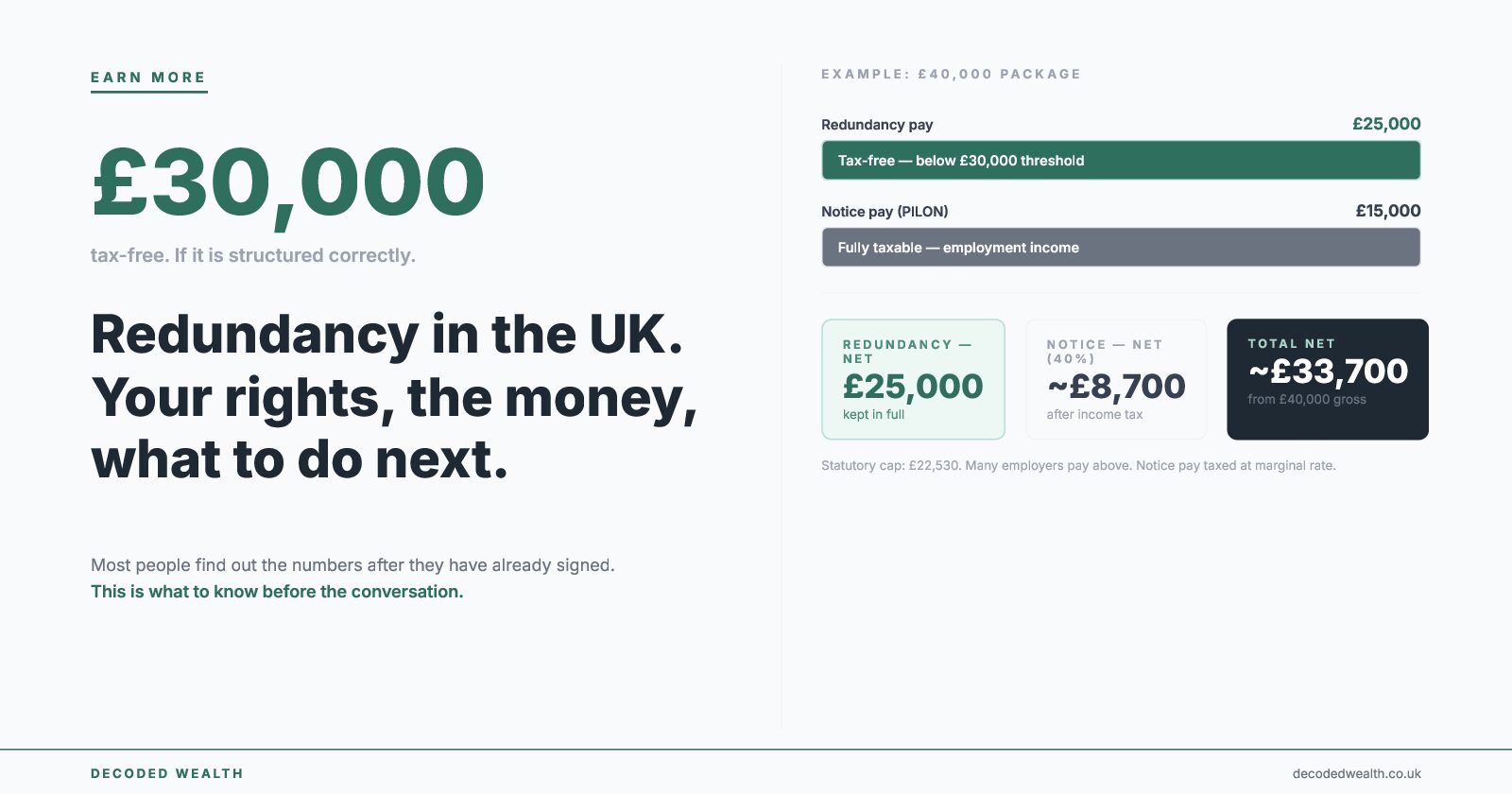

The first £30,000 of a genuine redundancy payment is free from income tax and National Insurance. This covers statutory and contractual redundancy pay combined. Everything above £30,000 is taxed as income.

Notice pay is different. It is not redundancy pay. Payment in lieu of notice, garden leave, worked notice: all of it is employment income, taxed at your marginal rate. This distinction matters more than most people realise.

Quick calculation: a real example.

A £40,000 package. Here is how the tax splits.

| Component | Gross | Tax treatment | Net (higher rate taxpayer) |

|---|---|---|---|

| Redundancy pay | £25,000 | Tax-free (below £30k threshold) | £25,000 |

| Notice pay | £15,000 | Taxed at 40% + 2% NI | approx. £8,700 |

| Total | £40,000 | approx. £33,700 |

Most people plan around £40,000. The money that actually arrives is closer to £33,700. The difference is not a surprise if you run the numbers first. It is a significant shock if you do not.

Pension during notice.

Employer pension contributions typically continue during notice periods, including garden leave. Confirm this in writing. Several months of lost employer contributions at exit is a real cost. It rarely comes up in the redundancy conversation unless you raise it.

What we found

When people close to us went through this, the financial shock was rarely what they had anticipated.

In one case the package was more generous than expected. But it was spent too quickly. No plan, no runway calculation, and the next role took longer than assumed. In another, the assumption that the whole amount was tax-free turned out to be wrong. Part of the package had been structured as enhanced notice pay. The tax bill arrived later and was a genuine surprise.

The consistent finding was this: the window between announcement and leaving date is more valuable than most people use. It is paid time. The people who handled it well treated it as a transition, not a waiting room. They reviewed entitlements in writing, confirmed pension status, updated their records, and began mapping what came next before the previous step had ended.

On the current market: some of what is happening is structural, not cyclical. Some of the roles made redundant in the past two years will not return in the same form. The people who handled redundancy well financially were the ones who identified quickly whether they were facing a job-search problem or a reskilling problem. The financial plan for each looks different. Confusing one for the other wastes both money and time.

What to do

Step 1. Get your entitlements in writing before you respond to anything.

Request a written breakdown before signing any settlement agreement. Identify how much is statutory, how much is contractual, and how much is notice pay. Each component has a different tax treatment. If the offer seems unclear or you want to know whether it is fair, Acas offers free, impartial guidance and can explain your rights before you sign.

Step 2. Confirm the tax position on your specific package.

The £30,000 threshold applies to genuine redundancy pay. Notice pay is fully taxed as income. Understand which parts fall into which category before you plan around a net figure. GOV.UK’s guidance on redundancy pay tax is clear and free. For complex packages or settlement agreements, Citizens Advice can review the terms at no cost.

Step 3. Check pension contributions during notice.

Ask in writing whether employer contributions continue, whether you are working the notice or on garden leave. If they stop, factor that gap into your planning. If you can direct some of the redundancy payment into your pension before leaving and you are within your annual allowance, this can be one of the most efficient uses of the money.

Step 4. Do not touch the redundancy payment until you have a plan.

Divide the net redundancy pay by your committed monthly costs. Not total spending. Committed costs. That gives you your runway in months. That number tells you how much urgency actually exists and what decisions you can afford to take slowly. You can read this article to

Step 5. Use the notice period actively.

Request references. Update employment records. Review your pension position. Start mapping what comes next. The notice period is paid time you control more than you might expect. Use it.

Step 6. Be honest about the type of problem you are facing.

If your role exists elsewhere and you have the skills to fill it, this is a search. If the role has changed substantially or been automated across your sector, this is a reskilling or pivot question. The financial plan for each is different. The longer it takes to identify which one you are in, the more runway you lose.

Before you sign: checklist

☐ Full package breakdown received in writing

☐ Redundancy pay separated from notice pay on the document

☐ Tax treatment of each component confirmed

☐ Net figure calculated, not gross

☐ Pension contributions during notice confirmed in writing

☐ Acas or Citizens Advice consulted if anything is unclear

☐ Runway calculation done before spending anything

Capital at risk. Investments can go down as well as up. This article is for informational purposes only and does not constitute financial advice. Decoded Wealth is not regulated by the FCA. Always do your own research before making financial decisions. This article may contain affiliate links. If you use them, we may earn a small commission at no extra cost to you.