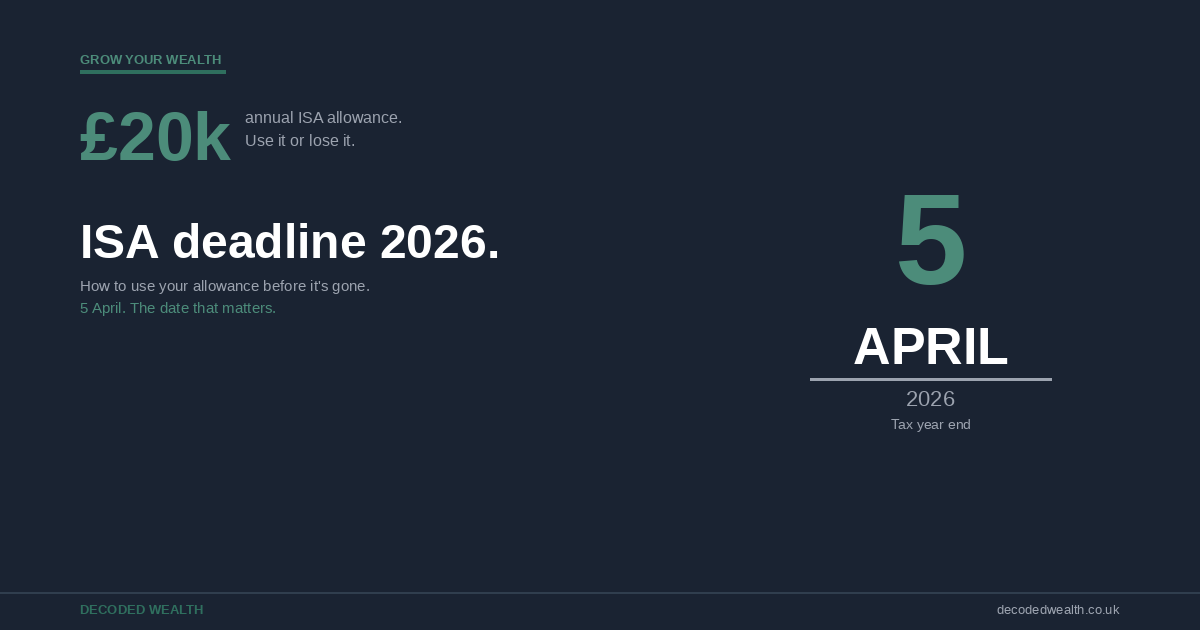

ISA Deadline 2026: How to use your allowance before it’s gone

Every year the 5th April comes around and a lot of people realise they’ve let their ISA allowance go to waste again. It’s not that they didn’t mean to use it. Life just got in the way.

If that’s you this year, you still have time. But not much. Here’s what to actually do before the deadline, and why it’s worth making a bit of effort to get it sorted.

What happens on 5th April

Your ISA allowance resets every tax year. You get £20,000 to put into ISAs — cash ISAs, stocks and shares ISAs, or a mix of both – without paying tax on any of the growth or income.

On 6th April, that resets to a new £20,000. But anything you didn’t use from the previous year just disappears. You can’t roll it over. You can’t ask HMRC nicely. It’s gone.

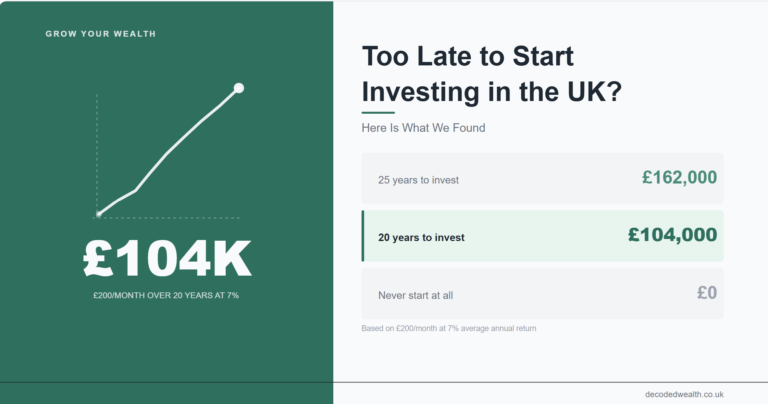

For most people this doesn’t feel like a big deal. But consider this: £10,000 invested in a stocks and shares ISA at a 7% average annual return over 20 years grows to roughly £38,000. All of it tax-free. Letting that allowance lapse isn’t a small thing – it’s a missed compounding opportunity that quietly costs you a lot over time.

The deadline is midnight on 5th April. Don’t leave it until the last minute – some platforms get busy and deposits can take a day to process.

First thing to do: find out how much allowance you have left

Log into your ISA provider’s app and look for your remaining allowance. Most of them show it on the main dashboard. If you have ISAs with more than one provider, remember the £20,000 is a combined limit across all of them – you can’t put £20,000 into each.

Only deposits count against your allowance. Interest earned or investment growth inside the ISA doesn’t eat into it.

What to do if you have spare allowance

If you’ve got money sitting in a current account or savings account that you don’t need for the next few months, this is the time to consider moving it into your ISA.

You don’t need to invest the full £20,000. Any amount is worth doing. Even a £500 top-up before the deadline gets that money into a tax-efficient wrapper where it can grow undisturbed.

For a cash ISA, it’s just a transfer. For a stocks and shares ISA, you deposit the cash and can decide later what to invest it in. The deposit is what uses the allowance.

If you already have an ISA

Log in and make a deposit. Most platforms allow same-day transfers from your bank account. That’s it.

If you don’t have an ISA yet

You can open one and make a deposit in the same day on most platforms. The account opening and the deposit both need to happen before 5th April. Don’t leave it until the evening of the 4th.

If you want to move to a better platform

You can transfer an existing ISA without it counting against your current year’s allowance — transfers are separate from contributions. If you also want to add new money, do that as a fresh deposit before the deadline.

The lifetime ISA deadline is the same date

If you’re between 18 and 39 and saving for a first home or retirement, the lifetime ISA gives you a 25% government bonus on contributions – up to £1,000 free money per year on a £4,000 contribution.

That deadline is also 5th April. The bonus is paid on what you contribute during the tax year, so missing the deadline means missing that year’s bonus entirely. If you’re eligible and haven’t yet contributed this year, this is probably your highest-priority financial task right now.

A 25% guaranteed return on your money is hard to find anywhere else. If you’re eligible for a lifetime ISA and haven’t maxed it this year, do that first.

What if you can only contribute a small amount

That’s fine. Most people don’t max out their ISA every year and that’s completely normal.

The point isn’t to hit £20,000. The point is to use whatever you can before the opportunity expires. A £1,000 top-up now, growing at 7% per year for 30 years, becomes around £7,600 – all tax-free. The compounding happens quietly, whether you’re watching it or not.

A quick checklist before 5th April

- Check your remaining ISA allowance in your provider’s app

- Work out if you have any savings you could deposit before the deadline

- If you’re eligible for a lifetime ISA, prioritise that first

- Make your deposit – don’t wait for the final days

- If you don’t have an ISA, open one today and make at least a small deposit

- Set a reminder for 6th April – your new £20,000 allowance opens that day

A note on timing if you’re investing

A common question this time of year is whether it’s a bad idea to invest right before the deadline, especially when markets feel uncertain.

For anyone with a time horizon of five years or more, the timing of a single deposit matters a lot less than simply being invested at all. The tax efficiency of the ISA wrapper is worth more than trying to pick a perfect entry point.

If you’re genuinely nervous, you can deposit the cash before 5th April to lock in the allowance and then decide how to invest it over the following weeks. The deposit is the important part.

Frequently asked questions

Can I contribute to more than one ISA in the same tax year?

Yes. Since April 2024 you can contribute to multiple ISAs of the same type in the same year, as long as your total across all ISAs doesn’t exceed £20,000.

What if I accidentally go over the limit?

HMRC will get in touch and you’ll need to withdraw the excess. It’s your responsibility to track your total contributions. Most providers will warn you before you go over.

Is the ISA transfer deadline also 5th April?

No. You can transfer an ISA at any time during the year. The deadline only applies to new contributions.

Can I open a junior ISA for my child before the deadline?

Yes. Junior ISAs have their own allowance of £9,000 per year and the same 5th April deadline. Parents, grandparents, or anyone else can contribute.

This article is for informational purposes only and does not constitute financial advice. Always do your own research before making any financial decisions. Capital at risk.